$1,140

111 Belle Street, Columbus, OH 43215(380) 333-9602Rent Savings

- 19 units available

- Studio • 1 bed • 2 bed

- Amenities

In unit laundry, Nest technology, Patio / balcony, Dishwasher, Pet friendly, New construction + more

Verified listing

Verified

TL;DR: Yes, you can still rent an apartment after an eviction. Here's the steps to take:

You can still rent an apartment even if you have an eviction on your record. While it may take more effort, strategies like focusing on private landlords, strengthening your credit, offering an extra security deposit, and being upfront about your situation can help you secure an eviction-friendly rental.

After all, according to Princeton University’s Eviction Lab, there are roughly 1 million–1.5 million eviction judgments each year in the United States.

The key is knowing where to look for an apartment that may be open to renters who have had past evictions, how to present yourself, and what landlords value most in a tenant.

Most eviction-related records affect renters for about seven years, but the exact timeline depends on whether the record appears in court filings, credit reports, or tenant-screening databases.

| Stage of the Eviction Process | Where It Appears | Typical Time It Can Affect You | What This Means for Renters | Source |

|---|---|---|---|---|

| Eviction filing (case filed in court) | Local court records; tenant-screening reports | Court records may remain public indefinitely, but tenant-screening reports typically include filings for up to 7 years | Even if the case was dismissed, some screening services still report the filing, which may affect rental applications. | CFPB – Tenant screening reports |

| Eviction judgment (court ruled in landlord’s favor) | Court records; tenant-screening databases | Usually reported for up to 7 years in screening reports | A judgment confirms the landlord won the case and may carry more weight than a dismissed filing. | CFPB – Tenant screening reports |

| Unpaid rent or eviction debt sent to collections | Credit reports (Equifax, Experian, TransUnion) | Up to 7 years from the original delinquency date under the Fair Credit Reporting Act | Landlords who check credit may see eviction-related debt even if they don’t check court records. | Experian – Collections on credit reports |

| Tenant-screening databases (background reports used by landlords) | Private screening companies used during rental applications | Typically up to 7 years, depending on the reporting company | Screening reports often combine court records, eviction filings, and rental debt into a single report. | CFPB – Tenant screening reports |

| Public court records | State or county court systems | May remain public indefinitely unless sealed or expunged | Even if tenant-screening reports stop showing the case, landlords may still locate it in public court records. | LawInfo – Eviction records |

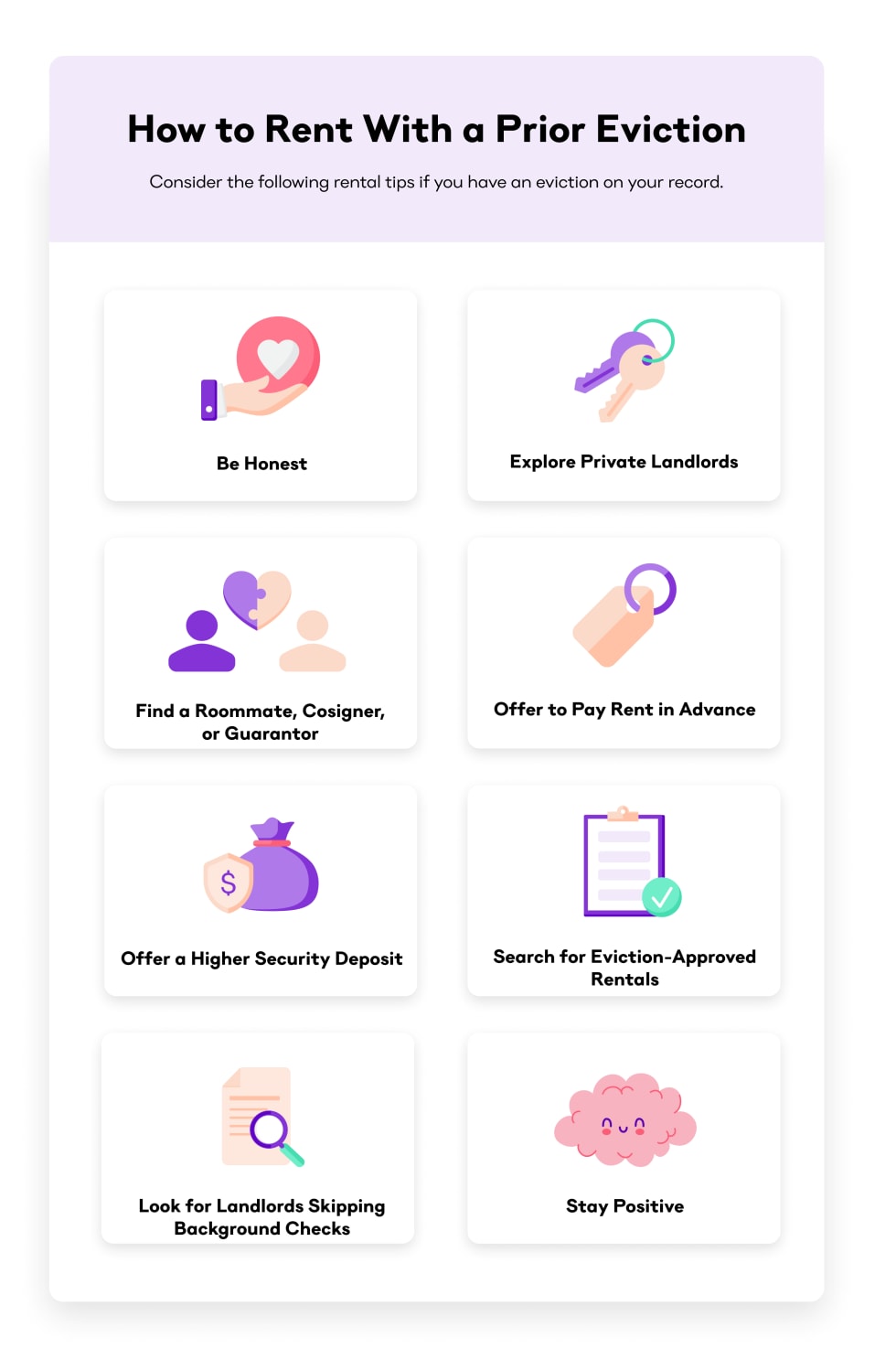

Here are a few practical steps to boost your chances of scoring a rental after you’ve previously been evicted.

An eviction may limit your options at first, which means being flexible is key. You may not land your dream apartment right away, but you can find a safe, affordable space that meets your needs.

Start by focusing on basics, such as budget, location, and move-in timeline, and worry less about extras like amenities or square footage. Once you rebuild your rental history, you’ll have more negotiating power for the next time you find an apartment.

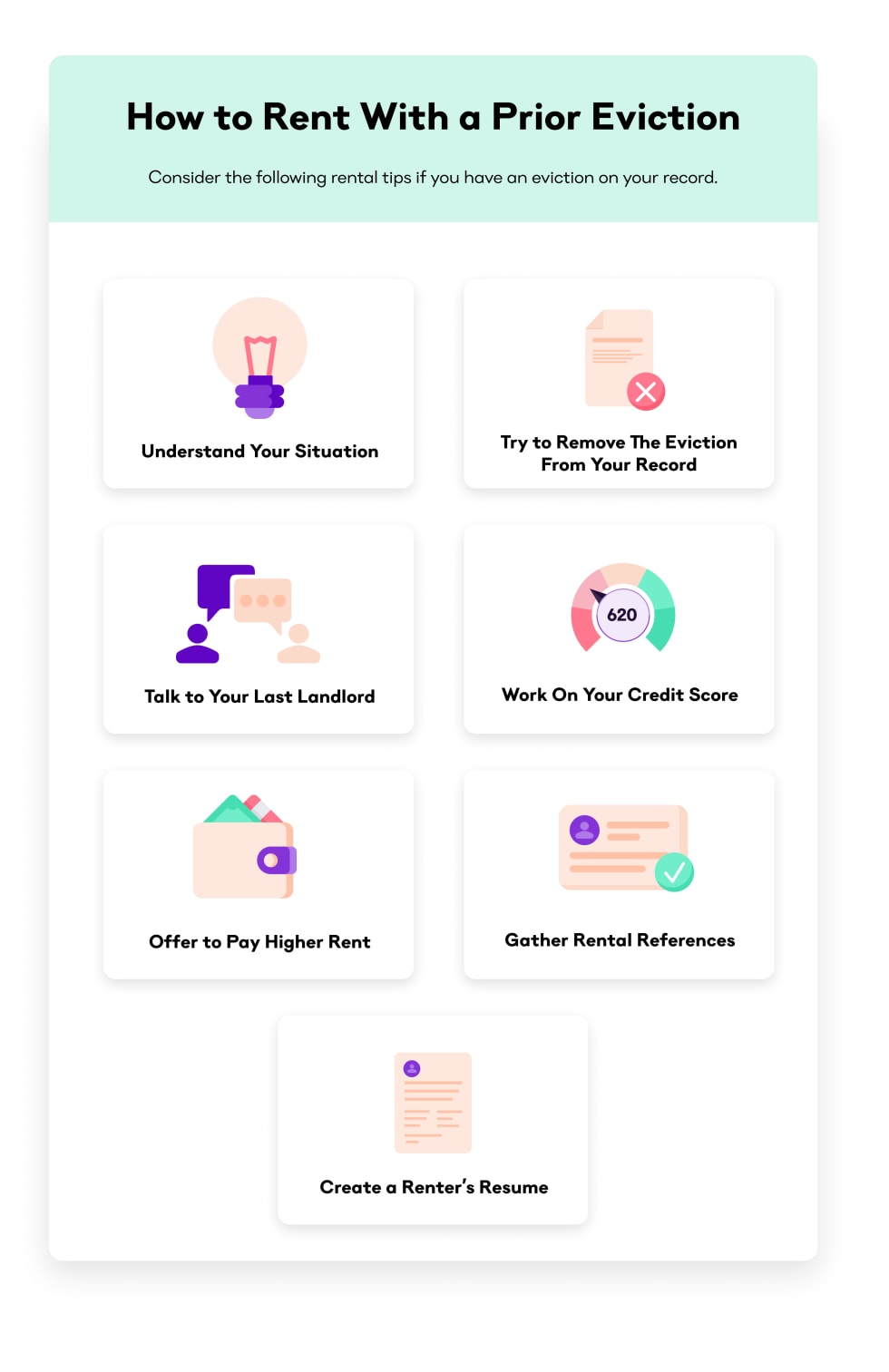

In some cases, you can have an eviction removed or “expunged” from your record, especially if it was filed in error or you’ve since resolved the issue. This process usually involves going back to court and proving that the eviction was inaccurate or unfairly reported. If you succeed, landlords and credit bureaus must update their records. Even if removal isn’t possible, showing proof that you attempted to resolve it can help demonstrate accountability to future landlords.

Large property management companies often have strict screening rules, and a past eviction may automatically disqualify you. Private landlords, on the other hand, may be more open to hearing your story and considering your current stability. When reaching out, be upfront about your history but emphasize what’s different now—steady income, stronger credit, or references. Building a personal relationship can go a long way in convincing a private landlord to take a chance on you.

Competition is fierce in big cities, and large complexes often have zero flexibility in their screening. Smaller towns, secondary neighborhoods, and locally owned buildings tend to be more open to negotiation.

These landlords are often more interested in filling vacancies quickly than rejecting applicants over past mistakes. Expanding your search radius can improve your odds of finding someone willing to work with you, while still landing you in a livable and affordable space.

Look for short-term or month-to-month apartments, as some of them may waive credit checks if you can prove you have the funds upfront.

Some landlords don’t run credit checks, especially if they own just one or two units and prefer to manage applications directly. These rentals can be great opportunities if your credit still shows eviction-related debt. But be cautious—“no credit check” listings are also where scams are most common.

Renters with past evictions are statistically more vulnerable to rental scams. Being aware of common red flags can help you avoid losing money or personal information.

Red Flags to Watch For:

Scammers often use phrases like:

These claims are often designed to pressure renters into sending money quickly.

Legitimate landlords will typically allow you to:

If someone insists you pay a deposit immediately to “hold the unit,” it may be a scam.

Some scammers steal photos from legitimate rental listings and repost them with a lower price to attract renters who feel they have limited options.

Warning signs include:

If you suspect a listing may be fake, try searching the photos or address online to see if the property appears elsewhere.

Be cautious if a landlord asks for payment through:

Most legitimate landlords accept checks, secure payment portals, or bank transfers after a lease is signed.

How to Protect Yourself:

If something feels suspicious, it’s better to walk away and keep searching.

If your eviction was tied to unpaid rent, clearing that balance can be a game-changer. Reach out to your former landlord, explain your situation, and ask if they’ll confirm repayment in writing. If you left on better terms than the court filing suggests, you may even be able to get a reference letter. A landlord vouching for your growth since the eviction can carry real weight with new property owners.

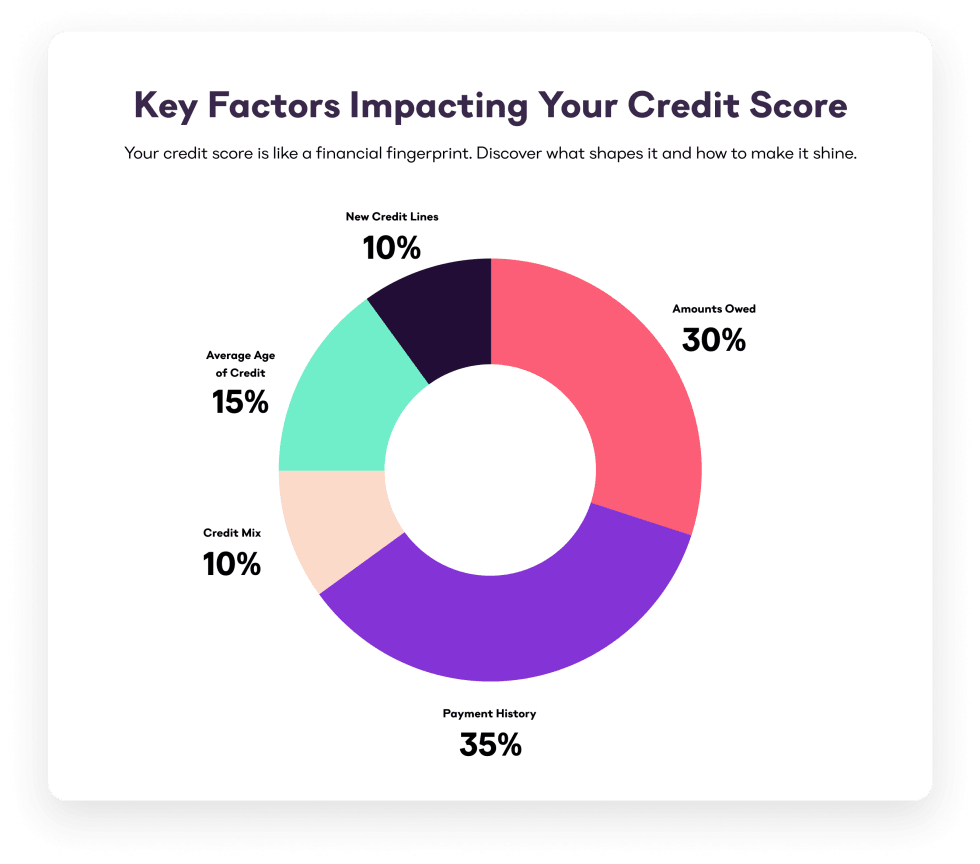

Your credit history plays a big role in the rental process, even more so if you’ve faced eviction. Start by pulling your free credit report to check for errors. If eviction-related debt is still listed, pay it down or negotiate a payment plan.

Then build positive credit history with on-time payments for utilities, credit cards, or loans. Over time, stronger credit can help offset your past eviction and give landlords confidence in your ability to pay rent reliably.

Few things reassure landlords more than guaranteed payment. If you have the savings, offering two or three months’ rent upfront can reduce their risk and improve your chances of approval.

Even if they don’t require it, making this gesture shows you’re serious and financially stable. Just make sure you can comfortably afford it. Don’t drain your safety net entirely, since you’ll need cash on hand for moving expenses and emergencies.

Security deposits are a landlord’s safety cushion, so offering more than the minimum can work in your favor. This approach shows you’re committed to protecting the property and making payments.

For example, if a landlord typically asks for one month’s rent, consider offering two. Since deposits are refundable if you leave the apartment in good shape, this strategy is often lower risk for you than paying higher monthly rent.

In competitive markets, offering slightly more than the listed rent can set your application apart. It demonstrates seriousness and helps landlords feel compensated for taking on perceived risk.

Just be cautious: this option can add financial strain over time. If you go this route, set a realistic budget and make sure you can sustain it. Pairing this strategy with proof of stable income helps reassure landlords that your offer is viable.

Gather the materials below to help prove to landlords that you're not a risky candidate for tenancy.

If you have an eviction on your record, it can help to briefly explain the situation to a prospective landlord. The goal is to be honest, show accountability, and highlight what has changed since the eviction. You can use our ready-to-copy template to write a short explanation letter.

Eviction Explanation Letter Template

Subject: Rental Application – Explanation of Prior Eviction

Dear [Landlord or Property Manager’s Name],

Thank you for considering my rental application for [property address].

I want to be upfront about a past eviction that appears on my record from [year]. At the time, I experienced [brief explanation of circumstances, such as job loss, medical issues, or another temporary hardship]. Unfortunately, this situation led to the eviction filing.

Since then, my situation has changed significantly. I am currently employed as a [job title] at [company name], where I have worked for [length of time]. My income is stable, and I have been consistently paying my bills and rebuilding my financial standing.

I have also taken steps to prevent this from happening again, including:

- [Example: paying off the previous rental balance]

- [Example: improving my credit score]

- [Example: maintaining steady employment]

If helpful, I’m happy to provide supporting documents such as:

- Proof of income

- References from previous landlords or employers

- Bank statements or credit reports

I understand that renting to someone with an eviction can feel risky, and I truly appreciate your willingness to review my application. I am committed to being a reliable and respectful tenant.

Please feel free to contact me if you have any questions or need additional information.

Thank you for your time and consideration.

Sincerely,

[Your Name][Phone]

[Email]

Tips for Writing an Effective Eviction Explanation Letter:

Strong references can help balance out a shaky rental history. Ask previous landlords, supervisors, or colleagues who know your reliability to write short recommendation letters.

Focus on your character, financial responsibility, and stability since the eviction. If you had an eviction during the pandemic, explain the context. Many landlords are sympathetic to COVID-era challenges.

Think of a renter’s resume as your “apartment pitch.” Include your employment history, proof of steady income, rental references, and any supporting documents like bank statements or pay stubs.

Organize this resume neatly in a single PDF so landlords can review it quickly. A polished renter’s resume helps shift focus away from your eviction and toward your qualifications, showing that you’re proactive, transparent, and serious about being a great tenant.

Living with a roommate can show a landlord greater financial stability. Cosigners and lease guarantors aren’t completely similar, but both can help make a potential landlord feel more confident renting to you.

While both cosigners and guarantors are held responsible for renters who fail to make rent payments, a cosigner has the right to reside on the property during the lease while a guarantor does not.

Honesty can go a long way when trying to rent an apartment while having an eviction on your record. Let the new landlord know what led to the eviction and how your financial stability has improved. More than that, a lack of honesty can cause issues that could even result in another eviction later. So it's important to be up front about your situation.

If you’re worried about eviction, acting early can make all the difference. Here are some steps that may help you stay in your home:

The sooner you take action, the more options you’ll have to avoid an eviction altogether.

An eviction is never easy to deal with, but it isn't the end of the world. You can still rent an apartment after being evicted and rebuild your rental history. So, don’t worry about how to rent with an eviction on your record. Instead, figure out where to get started in your apartment search by checking out Apartment List’s online quiz today!

Want more help insight into removing evictions from your record? Check out this fantastic, detailed guide on exactly how to phrase your eviction appeal from Attorney Robert Flessas:

It can take up to seven years for an eviction to disappear from your credit report.

You’ll need to petition the court to have the eviction removed. However, the court will only remove it if you're disputing an inaccurately reported eviction.

Eviction can impact your credit if there are fees associated with the eviction that go to collections. Does eviction stay on your record? Well, it can, again, depending on what is reported.

Start by being honest. If your landlord is open to negotiating, explain your prior eviction and the steps you've taken to prevent one in the future. Consider offering a higher security deposit, paying more in rent, staying on a month-to-month lease or short term lease, offering rental references, or finding a cosigner to help your prospective landlord feel at ease renting to you.

Yes. It may take more time and effort, but many landlords are open to renting to tenants with past evictions, especially if you show financial stability.

Most evictions stay on your credit for 7 years, but their impact lessens over time, especially if you rebuild good payment history.

These are rentals where landlords are willing to consider applicants with past evictions, often in smaller complexes or managed by private owners.

Yes. If you repay past debts, landlords are far more likely to view you favorably—and you may even be able to remove the eviction record in some cases.

In unit laundry, Nest technology, Patio / balcony, Dishwasher, Pet friendly, New construction + more

In unit laundry, Patio / balcony, Pet friendly, Stainless steel, Walk in closets, Gym + more