Remote Work Revolution Gives Rise to a New "Untethered Class"

Overview

- The remote work experiment of the past year has constituted a step change in a long-term trend of remote work becoming increasingly common. Many Americans who worked in offices before the pandemic are likely to continue working remotely even after it subsides. By severing the link between job choice and housing choice, remote work could have a profound impact on where Americans choose to live.

- We estimate that nearly one-in-three jobs in the U.S. are in occupations that can be performed remotely, and in some places, the share is much higher. In the San Jose metro encompassing Silicon Valley, 46 percent of jobs are remote-friendly.

- Since jobs are not the only factor that keep people rooted, we propose a new concept -- the "untethered class," composed of workers who are employed in remote-friendly occupations, but also are not tied down by homeownership or family obligations. As we’ve defined it, the untethered class consists of 8.7 million workers accounting for 5.6 percent of the total American workforce, but with significant regional variation.

- The San Francisco metro has the highest share of untethered workers at 13.5 percent, followed closely by neighboring San Jose. The remainder of the top 10 consists primarily of "superstar cities" that are characterized by their high housing costs, including Los Angeles, Seattle, New York City, and Boston.

- The untethered class are highly-educated and high-earning, and with a median age of 32, many are likely on the precipice of settling down. The untethered class are also more likely than the general population to be living in a different state than where they were born, indicating a propensity to relocate.

- Given that so many untethered workers are living in the nation’s most expensive housing markets, many may choose to relocate to markets where they can afford to purchase homes and raise families more comfortably. While such a trend would be unlikely to lead to the demise of superstar cities, it has significant potential to reshape the markets that the untethered class moves to.

Introduction

The remote work experiment of the past year has constituted the most rapid shift to working life in decades. However, the rise of remote work predated the pandemic -- from 2005 to 2018, the number of Americans working from home grew by 76 percent, meaning that the fastest growing commute category over that timespan was no commute at all. As vaccine distribution gains momentum, we seem to be fast approaching a day when working in an office will again be safe, leading many to ponder the future of remote work. While many who are currently working from home will undoubtedly return to an on-site setting, a number of high profile companies have already announced plans for permanent changes to offer remote flexibility to their employees.

Roughly one-in-three employed adults works in an occupation that can feasibly be performed remotely. If a significant share of these workers are allowed that remote flexibility by their employers, it could have drastic implications for where Americans choose to live, severing a previously unshakable link between job choice and housing choice. That said, jobs are not the only factor that ties people to the places they call home. This raises a number of crucial questions. How will companies handle remote work post-pandemic? Which industries and occupations will be most disrupted? How might remote flexibility impact the location preferences of those given the option to work anywhere? What impacts will remote work have on cities and who will be the winners and losers? These are all questions that our team will be researching in the coming months.

In this report, we begin that research by taking a rigorous and nuanced look at perhaps the most fundamental question poised by the remote work revolution -- which workers would be most likely to actually relocate if given the opportunity to live anywhere with a good internet connection? We propose an answer in the form of a newly defined segment of the workforce that we refer to as the “untethered class.” In addition to working in remote-friendly occupations, the untethered class are renters, meaning that they are not tied down by homeownership. Nor are they tied down by school age children or a spouse with a non-remote-friendly job. If given the option for permanent remote work, the untethered class would be free to pack up and move as they please, representing the leading edge of what has the potential to be a new era of geographic mobility in the United States.

The untethered class contains 8.7 million American workers, comprising 5.6 percent of the national workforce, but as we show below, this share is much higher in superstar cities such as San Francisco, Austin, Seattle, Washington, D.C., and New York City. Although they earn above-average incomes, untethered workers in these metros face the nation’s highest housing costs, which could push them to consider moves to more affordable markets as they prepare to settle down. Read on to learn more about the untethered class and their potential to reshape the urban geography of the United States.

What occupations can be done remotely?

The first step in defining the untethered class is to identify those workers whose jobs can be done remotely. Over the course of the past year, as the ability to work remotely has emerged as an important predictor of both employment and health outcomes, a number of researchers have tackled this question. We build on this prior research to construct our classification. Specifically, we start with definitions devised by University of Chicago economists Jonathan Dingel and Brent Neiman, and then apply our own modifications designed to identify occupations for which remote work is not just possible today but for which it will continue to be viable post-pandemic.

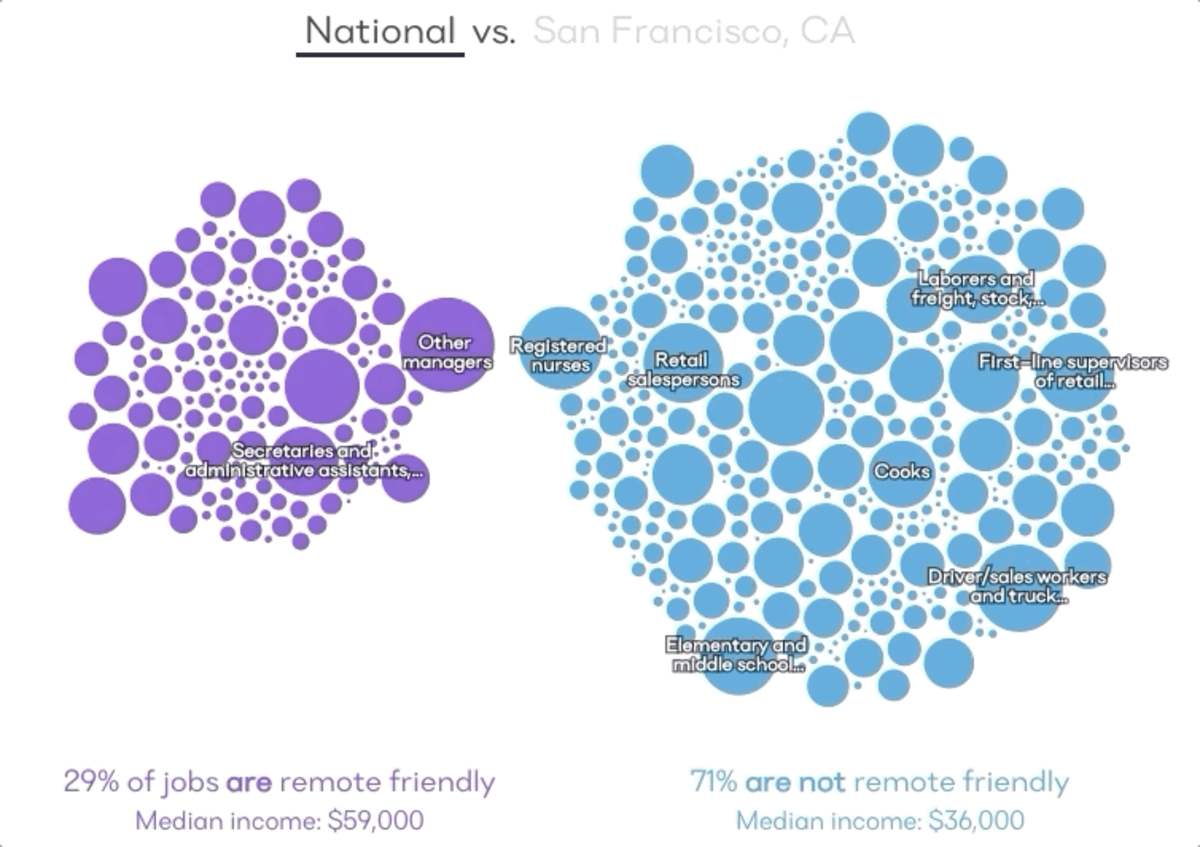

According to our classification 29 percent of the adult workforce is employed in remote-friendly occupations. Some of the most common remote-friendly occupations include administrative assistants, accountants, and software developers, while on the non-remote-friendly side, examples include nurses, retail salespersons, and teachers. Remote-friendly occupations tend to be higher-paid, with a median income of $59,000, which is 64 percent higher than the $36,000 median for those workers whose jobs require them to be on-site.1

However, the share of the workforce with the potential to go remote varies considerably by location. Metro-level breakdowns tell us a great deal about the distinct local economies of different parts of the country, as made clear by the example of the San Francisco Bay Area. In the San Jose metro, home to Silicon Valley, 46 percent of employed adults have remote-friendly jobs, the highest share of any metropolitan area in the country. San Jose also has the nation’s widest gap between the median income of those who can work remotely ($118,000) and those who cannot ($45,000), a premium of 162% for remote-friendly occupations. The labor market in the neighboring San Francisco metro is similar -- 42 percent of the workforce has remote-friendly jobs, and those workers earn a median income of $98,300, which is 113% more than the $46,000 median income for San Francisco based workers whose jobs must be done on-site.

The degree to which the tech industry dominates the Bay Area is evidenced in this occupational data by the stark overrepresentation of software developers. Across the U.S. as a whole, just 1.1% of working adults are software developers, but that figure spikes to 9.7% in the San Jose metro and 4.4% in San Francisco, making it the single most common occupation in both metros. The lure of high-paid tech jobs has been drawing highly-educated workers to the Bay Area from around the country for decades. However, new housing construction in the region has been woefully scarce, and this imbalance in supply and demand has created the nation’s most acute housing affordability crisis. As a result, many low- and middle-income workers have been pushed to the farther reaches of the region in search of greater affordability.

Stockton, CA -- which lies 80 miles east of San Francisco -- illustrates this trend. Just 23 percent of workers living in the Stockton metro are employed in remote-friendly occupations, the 4th lowest share among the nation’s 100 largest metros. In prior research, we found that Stockton ranked #1 for the share of the workforce who qualify as “supercommuters,” travelling more than 90 minutes each way to work. Even among Stockton workers whose jobs are remote-compatible, the median income is just $51,000, roughly half that of remote-friendly workers in the San Francisco and San Jose metros. Software developers comprise just 0.7 percent of Stockton’s workforce, while “Driver/sales workers and truck drivers” is the metro’s most common occupation.

The Bay Area is just one important example of how this occupation-level breakdown can illuminate local labor and housing market dynamics. Explore the interactive graphic below to delve further into these geographic differences. This tool also allows you to toggle the remote-friendly status for individual occupations to devise your own classification and see how results change.

Not all those in remote-friendly occupations are part of the “untethered class”

Newfound remote work flexibility may sever the tie between labor markets and housing markets for a significant portion of the workforce, but there are other tethers that root people to the places where they live. In this report, we go beyond just a remote-friendly classification in order to identify the workers who are least rooted, considering not just occupation, but also family ties and homeownership status. We define the “untethered class” of workers as those who meet the following criteria:

- Works in a remote-friendly occupation

- Lives in a renter household

- Lives without a spouse or with a spouse who is either not working or working in a remote-friendly occupation

- Has no school-age children living in the household

According to our definition, the untethered class consists of 8.7 million workers and accounts for 5.6 percent of the American workforce. If geographic flexibility in their working arrangements outlasts the pandemic, these untethered workers will face no significant barriers in choosing to live wherever they please. The ongoing remote work revolution will have a significant impact on America’s urban geography, and the untethered class represents the leading edge of this trend. Their behavior over the next few years will serve as a harbinger for longer-term implications.

Of course, while we consider our definition of untethered workers to be a useful construct, it is not meant to be absolute. Many remote-friendly workers who own homes or have familial tethers may also be poised to move in response to newfound geographic flexibility, they just face some additional friction in doing so. The above graphic illustrates this nuance more clearly, presenting a full breakdown of the national workforce based on which of our untethered criteria they meet (for this purpose, we combine the constraints on spouses and children into a single “family tether”). This graphic is also interactive, allowing you to explore regional differences, which we delve into further below.

This view illustrates how the untethered class expands if certain constraints are loosened. For example, 10.4 percent of the workforce are remote-friendly homeowners with no familial tethers. Selling a home may be more difficult than choosing not to renew a lease, but by no means is homeownership an absolute restriction on mobility, particularly over the medium- to long-term. Nearly one-in-five American workers are either fully untethered, or tethered by either family or homeownership, but not both. This is similar to the share that are “fully tethered,” meaning that they are tied down by not just a non-remote-friendly job, but also by homeownership and family.

Who is part of the untethered class?

The potential of the untethered class to usher in a new era of geographic mobility is illuminated even more clearly when we explore further attributes of the workers that comprise this group. The interactive table below presents key demographic characteristics for the untethered class, with comparisons to the broader group of all workers employed in remote-friendly occupations, as well as to the full population of employed adults. This tool allows you to toggle the four filters that we apply to arrive at our definition of untethered workers, in order to see how results change when the criteria are loosened.

Nationally, the untethered class as we’ve defined it has a median income of $50,000. Although this is 22% higher than the overall median for all workers, it is also 15% less than the median for remote-friendly workers broadly. The median age of the untethered class is 32, a full decade younger than the overall median of the workforce as a whole. 57 percent of untethered workers have a 4-year college degree or higher, meaning that the untethered class is the most highly educated of the three groups shown in the table. The untethered class is also most likely to have been born in a different state than where they currently reside, an important fact to keep in mind as we consider this group’s propensity to relocate.

The demographic composition of the untethered class indicates that it is composed of highly educated workers who are in the early to mid stages of their careers. They are earning above average incomes, but have yet to attain homeownership, a goal which our prior research shows is still held by the vast majority of millennial renters. As these workers move into a stage of life where they are likely preparing to settle down, having the ability to work from anywhere could have a significant impact on where they choose to do so. And as we show below, the untethered class is heavily concentrated in some of the most expensive housing markets in the country, a fact which is likely to impact their future decision making.

Where does the untethered class live?

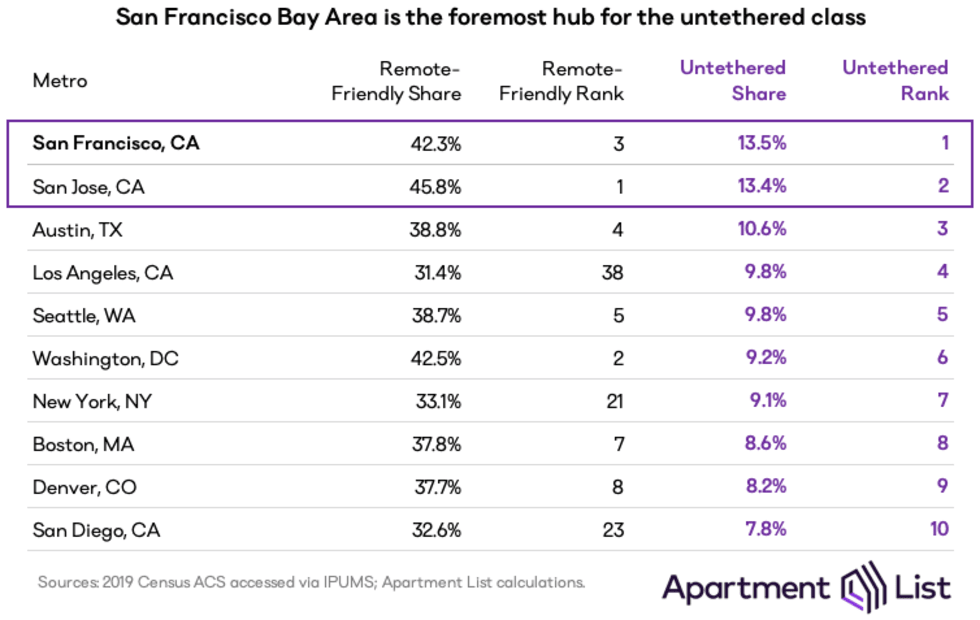

As with remote work broadly, the prevalence of the untethered class varies widely by metro, and here too, the Bay Area is the epicenter. San Francisco ranks first, with the untethered class comprising 13.5 percent of the adult workforce, and San Jose comes just behind at number two, with 13.4 percent of workers being untethered.

Beyond the Bay Area, the top 10 metros for untethered workers is rounded out by a list of “superstar cities” that will be familiar to observers of urban economics. Superstar cities are characterized by strong local job markets that have been attracting high-income households for decades, combined with constraints on new housing supply that have led to high local housing prices which crowd out low-income households. We explored this pattern as it pertains to the Bay Area in the section above, but the same dynamic is at play to varying degrees in all of the metros where untethered workers are most concentrated.

This is not a coincidence; a concentration of high-paid knowledge sector jobs is a defining feature of superstar cities, and remote work compatibility is far more prevalent in these jobs than in the overall economy. Meanwhile, the other key characteristic of superstar cities -- high housing costs -- has kept homeownership out of reach even for many of those earning above-average incomes. Across the five metros with the highest share of remote workers -- all of which also make the top ten for untethered share -- 63.7 percent of remote-friendly workers live in homeowner households. This is slightly lower than the national homeownership rate, and well below than the 70.8 percent rate for remote workers nationally. In other words, housing costs in superstar cities are causing a greater share of the remote-friendly workforce to remain untethered as they continue to rent. If these housing affordability issues remain unaddressed, superstar cities may lose many of their untethered workers to other cities where those workers can afford to settle down and raise families more comfortably.

In areas with a high share of remote-friendly workers, those workers are also less likely to be tied down by family tethers. In the five metros with the highest remote-friendly shares, 22.0 percent of those workers are tethered by a spouse who works in a non-remote-friendly occupation, compared to 29.1 percent nationally. Remote-friendly workers in these metros are just barely less likely to be married, but it is more likely that their spouses also work in remote-friendly occupations.

These patterns create a sort of compounding effect, in which each of the factors we consider in our definition of untethered workers conspire such that the untethered class is significantly overrepresented in superstar cities. The ten metros where the untethered class is most prevalent contain 36 percent of all the nation’s untethered workers, despite the fact that they account for just 21 percent of the nation’s adult workforce as a whole.

Again, the Bay Area serves as an important case study. The 42.3 percent share of remote-friendly jobs in San Francisco is 1.8x greater than the 22.9 percent share in Stockton, which represents the far edge of the region’s commuting radius. However, San Francisco’s untethered share of 13.5 percent is 3.6x greater than that of Stockton, which ranks 84th for the prevalence of untethered workers at 3.7 percent. This is largely driven by homeownership. In the San Francisco metro, just 55.8 percent of remote-friendly workers are homeowners, while in Stockton, the remote-friendly homeownership rate is 66.9 percent, despite the fact that the median income of remote-friendly workers in Stockton is just $51,000, compared to $98,300 for remote-friendly workers in San Francisco. In fact, the ability to afford homeownership is likely the reason that many of these workers chose to live in Stockton, even if it may have required a burdensome commute.

Going forward, it is likely that many employers will adopt hybrid working arrangements in which employees are given some remote flexibility, but are still required to come to an office on a less frequent basis. Some workers would likely be willing to bear an even longer commute than the one from Stockton to San Francisco, if the trip were not being made daily. This could lead to a future in which the commuting ranges of costly superstar cities may expand even further.

Despite the compounding effect described above, the list of metros with the highest concentration of untethered workers does not fully overlap with the list of metros where remote-friendly jobs are most common. In Los Angeles, for example, just 31.4 percent of the workforce is remote-friendly, only slightly above the national average and ranking 38th among the 100 largest metros. However, the L.A. metro has the lowest homeownership rate for remote-friendly workers and the 4th lowest rate of familial tethers among remote workers. Because of these factors, it jumps to 4th in the ranking of untethered workforce share. A similar dynamic plays out in the New York City and San Diego metros, neither of which makes the top 20 for remote-friendly workforce share.

Conversely, Des Moines, IA -- a major hub for the insurance industry -- has the 6th highest remote-friendly share, but ranks 58th for untethered share, due to an above average homeownership rate among remote-friendly workers, as well as the fact that an above average share of those workers having school age children. Similarly, the Raleigh, NC metro, also known as the “Research Triangle,” ranks 27th for untethered workers, despite having the 9th highest remote-friendly share. These examples help to illustrate how our definition of untethered workers is more nuanced than simply looking at the share of the workforce in remote-friendly occupations. Although remote-friendly jobs are actually notably more prevalent in Des Moines and Raleigh than in Los Angeles, we expect that L.A. has a higher likelihood of facing remote work related out-migration.

Conclusion

The remote work experiment of the past year has not been without its difficulties, and many companies will likely reopen offices when it is safe to do so. That said, even if the pendulum swings back somewhat, we are still in the midst of a significant step change in the long-term trend of remote work becoming increasingly common. As technology continues to improve, a growing number of jobs are likely to become remote-compatible, and as companies move through the growing pains of learning best practices for a remote workforce, any recent road bumps will be smoothed out. Furthermore, there is good reason to believe that employees will increasingly view remote flexibility as a valuable perk, such that employers will face pressure to offer that flexibility in order to remain competitive in attracting the best talent.

In the coming years, the geographic preferences of remote workers could have significant ramifications for housing markets across the country. If the untethered class decides that they are fed up with the high housing costs in superstar cities, they could spur a wave of migration to more affordable markets. Although superstar cities are unlikely to face a mass exodus, even a modest outflow has the potential to disrupt smaller markets. At the same time, a growing number of cities are making concerted efforts to attract remote workers, seeing an opportunity for economic development.

The full implications of the remote work revolution will take years to become fully evident, and there are many important and interesting facets of this trend that require further research, and which our team will be investigating closely. As a first step, we hope that our definition of the untethered class will serve as a useful framework for researchers, policymakers, and industry leaders as they seek to understand and plan for a future in which remote work is commonplace.

- In their paper “How Many Jobs Can be Done at Home?,” Dingel and Neiman devise an occupation classification based on the Work Context and Work Activities Surveys from the Department of Labor’s ONET program. While this classification was specifically designed within the context of the pandemic, our purpose is slightly different -- to identify occupations for which remote work will continue to be viable post-pandemic. This subtle difference is made clear by the example of teachers; although the pandemic has shown that remote learning is possible, getting teachers back to the classroom has been a flashpoint for school districts across the country. Our classification of remote-friendly occupations begins with the criteria outlined by Dingel and Neiman, but we then apply an additional filter, such that occupations where “training and teaching others” or “assisting and caring for others” are very important are considered non-remote-friendly. We then map occupation codes and their respective remote-friendly flags from ONET to the Census’ American Community Survey, in order to better understand the demographics of different groups of workers.↩

Share this Article