Student Debt and Millennial Homeownership

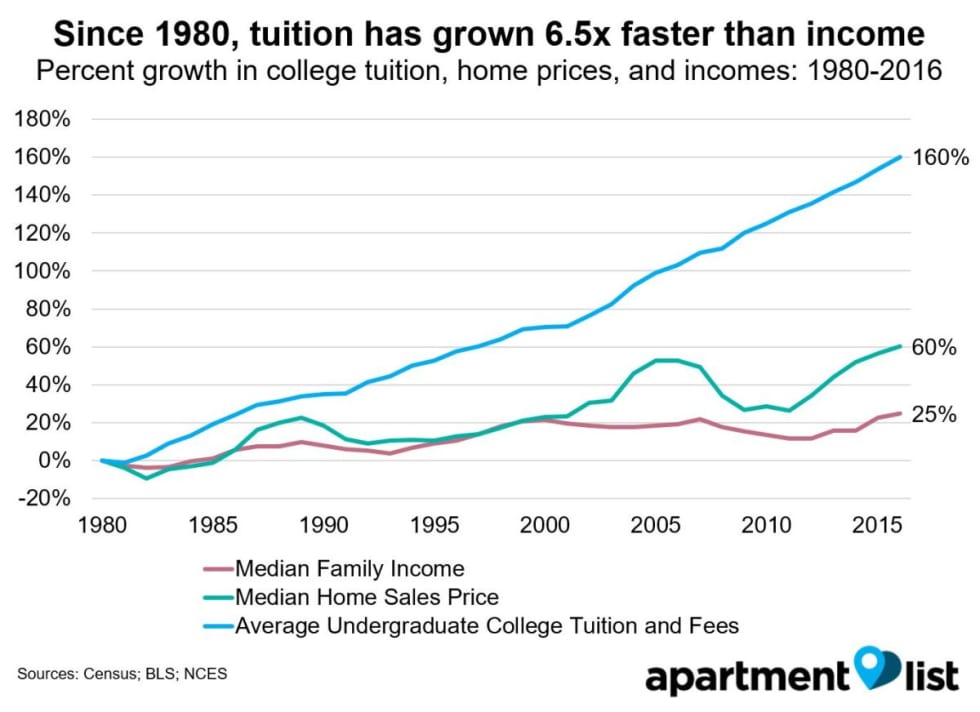

Since 1980, the real median family income has grown by 25 percent, while the median home price has grown by 60 percent, and the average cost of undergraduate tuition has jumped by 160 percent.

Results from the Apartment List Renter Survey indicate that recent college graduates with no student debt have, on average, $10,370 in savings for a down payment and expect $3,570 more in down payment assistance from their families, while recent college grads with student debt have less than half that combined amount, and millennials without a college degree less than one-fourth.

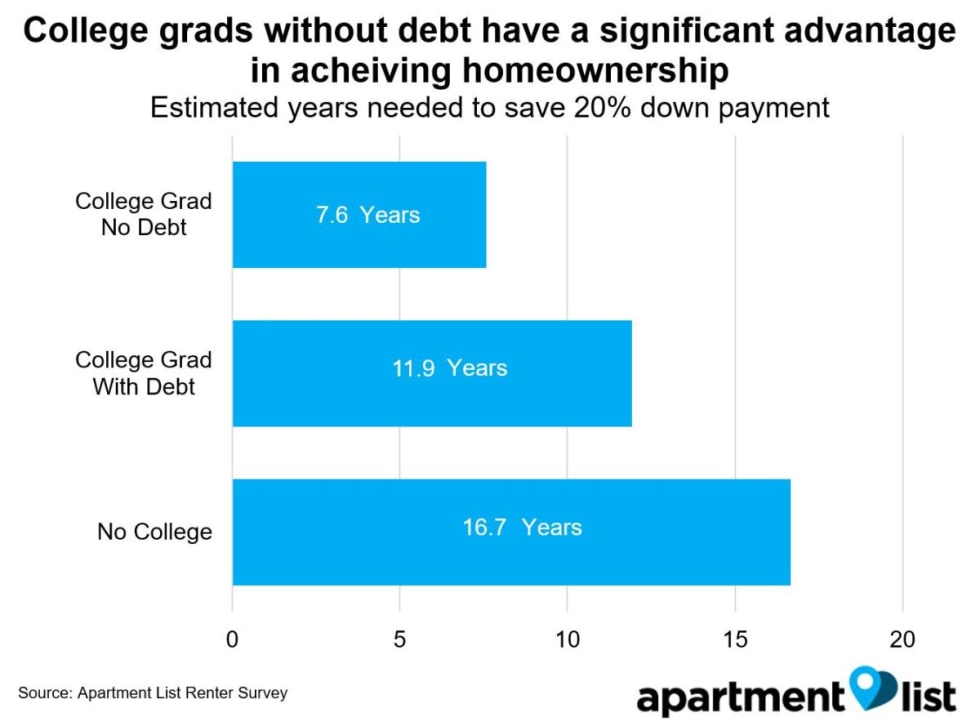

Homeownership is a distant goal for most millennials. We estimate that college grads without debt need 7.6 years to save a 20 percent down payment for a condo, compared to 11.9 years for college grads with debt, and a staggering 16.7 years for those without a college degree.

In many parts of the country, saving could take substantially longer; renters without college degrees will need well over 20 years to save for a down payment on a condo in Austin, San Francisco and Los Angeles.

Intro

Millennials represent the largest generation in our nation today, and their ability to purchase homes has broad implications for the housing market and society as a whole. Unfortunately, several long-term trends, including the explosion of student debt, make it increasingly difficult for millennials to save for a home. From 2005 to 2015, the average student debt burden of graduating college seniors increased by 70 percent.

Analyzing responses to our Apartment List Renter Survey from over 11,000 millennials across the U.S., we found that indebted college graduates are saving significantly less for a down payment compared to those without debt, while those without a college degree save even less.

As incomes have stagnated, tuition and home prices have risen sharply

When discussing the impact of student debt on the ability of millennials to save for homeownership, it is important to consider historical context. For decades, the cost of a college education has been skyrocketing, while incomes have grown much more modestly. Since 1980, the median family income, adjusted for inflation, has increased by 25 percent. Over the same period, the median home price grew at 2.4 times that rate, an increase of 60 percent, and the average cost of undergraduate college tuition grew 6.5 times as fast as the median income**, increasing by 160 percent.**

It’s important to note that student debt does not necessarily increase at the same rate as tuition, as many students receive scholarships and other forms of financial aid. That said, figures that focus specifically on student debt are equally alarming. A study last year by the Federal Reserve Bank of New York found that students graduating in 2015 with loans had an average student debt of $34,000, a 70 percent increase from 10 years earlier. The study notes that “having student loans dampens homeownership rates at every level of education, and higher debt balances are associated with even lower homeownership rates.”

As college has gotten more expensive, attendance has also increased, with the share of Americans 25 years of age to 29 with a bachelor’s degree or higher reaching 36.1 percent in 2016, up from 22.5 percent in 1980. Many students are likely lured into higher education by the promise of greater future earnings, as the income gap between those with and without college degrees has widened. In 1980, the average high school graduate earned roughly 71 percent as much as the average college graduate, but by 2010 that figure had fallen to 57 percent.

Structural changes in the labor market explain part of that earnings gap, with a shift in the U.S. away from manufacturing and toward a knowledge and service economy. While skills learned in college may be increasingly important to today’s jobs, some experts argue that we are experiencing the results of large-scale credential inflation, with college degrees now needed for jobs in which they previously weren’t necessary. This argument derives from the notion that employers value a college degree primarily as a signal of a good worker, and that the actual knowledge and skills learned do little to prepare students for the workplace.

College grads with debt are saving less for a downpayment

The fact that students feel increasing pressure to attend college to compete in today’s economy, coupled with the growing cost of a college education, has important implications for the housing market, as millennials with student debt burdens face increased difficulty in saving for homeownership. Data from the Apartment List Renter Survey shows that college graduates with debt are saving significantly less toward a down payment compared to those without debt. That said, those without a college degree are least prepared for homeownership.

.

We divide respondents into three groups: (1) those with a bachelor’s degree or higher and no student debt; (2) those with a bachelor’s degree or higher with student debt; and (3) those who did not graduate college, including respondents who attended “some college” but did not attain a bachelor’s degree. Millennials in the three groups report that they want to achieve homeownership at essentially the same rate, with 79 to 80 percent of each group stating that they plan to purchase a home in the future.

Despite sharing a similar yearning for homeownership, savings rates across the three groups vary widely. We find that college grads without debt have, on average, $10,370 saved for a down payment and expect to receive an addition $3,570 in assistance from family. Meanwhile, the average college grad with student loans has saved $4,320 and expects $2,220 in assistance from their families. Note that the difference in expected assistance in family implies that students who take on student debt tend to come from less privileged socioeconomic backgrounds. Those without a college degree have saved $2,240 on average, with expected assistance of $1,130 from their families. Thus, compared to college grads without debt, those with debt have less than half the combined down payment savings and expected assistance, while those without a college degree have less than one-fourth.

This same pattern holds true in the amount that each group saves toward a down payment each month; college grads without debt save $60 more each month than those without debt, and they save $120 more than those without a college degree. While those differences may not seem huge, they add up. Over the course of 10 years, those monthly gaps add up to total differences of $7,480 and $14,230, respectively, without even factoring in interest earned on savings.

College grads with debt need an extra 4.3 years to save a 20 percent down payment on a condo

To illustrate the implications of the difference in saving rates, consider how long it would take each group to save for a down payment on a condo. We estimate how long it would take each group to save enough for a 20 percent down payment on a condo priced at the national median of $222,000, based on the average amount that each group currently has saved, the amount of assistance they expect to receive and the amount they are saving on a monthly basis. Our calculation accounts for projected growth in home prices and returns on savings; it also accounts for growth in wages due to inflation.1

We find that even an initial step into homeownership - obtaining a mortgage - would require many years of saving for all three groups of millennials. Even recent college grads without debt, the group best situated to save for a down payment, need 7.6 years to save 20 percent of the median condo price. Recent college grads with debt need an additional 4.3 years, or 11.9 years in total, while millennials without a degree need an additional 9.1 years, or 16.7 years total. In other words, a 25-year-old who did not attend college would not have enough saved for a down payment until she is 42; assuming a 30-year mortgage, she would be paying off her home loan into her 70s.

In some metros, saving for a down payment could take 20 years or more

The calculation above assumes, for simplicity, the same national median condo price for all respondents. Since, in reality, real estate prices vary widely across the nation, we repeated the calculation at the metro level, using local median condo prices for 20 of the nation’s largest markets.

We find that in Austin, San Diego, San Francisco, Los Angeles and Denver -- one-fourth of the metros we analyzed -- millennials without a college degree would need more than 20 years to save enough for a down payment. In San Francisco, college grads with debt would need as much as 27 years! Such lengths of time suggest that many millennials in these metros may never actually achieve homeownership (or may need to move elsewhere to do so).

Just like at the national level, recent college grads without debt tend to fare better, but in nearly half of the metros we examine, these millennials still require more than a decade to save a 20 percent down payment on a condo. Meanwhile, for those without a bachelor’s degree, Tampa and Miami are the only metros where millennials need less than a decade to save the down payment. At the other end of the spectrum, homeownership is a slightly more realistic goal for millennial renters in Philadelphia, Minneapolis and Dallas; recent college grads with debt need 7.6 years, 7.9 years and 8.1 years, respectively, in those cities, to save the 20 percent down payment.

Conclusion

Much has been made of when -- and if -- the millennial generation will begin purchasing homes on a wide scale. Unfortunately, data from the Apartment List Renter Survey suggests that most millennial renters still have a long way to go before having enough saved to afford a down payment. More worrisome, recent college graduates’ savings appear to be diminished when they have student debt. Although this almost surely reflects differences in background -- millennials who have accumulated more savings are less likely to have needed to borrow for college expenses in the first place -- it also suggests that student debt plays a role in hampering the ability of millennials to save for a down payment.

Millennials also face a housing market with a historic shortage of starter home inventory, as well as recent changes to the tax code that make homeownership less attractive. Furthermore, the best job opportunities are increasingly clustered in a handful of superstar cities, where real estate prices are far above the national average, making homeownership an even more distant dream.

For most American homeowners, their house is their largest financial asset, and homeownership has long been the key source of wealth creation for many American families. Large student debt burdens and a lack of high-paying job opportunities for those without college degrees will likely become a source of deepening wealth inequality in America as homeownership moves increasingly out of reach for those from less privileged backgrounds.

Methodology

Responses to the Apartment List Renter Survey were collected from October 2016 to December 2017. Responses reflected here are limited to millennial renters between the ages of 22 and 35, with current students excluded. Age distributions are similar across education categories; the “College Grad No Debt” sample has a median age of 26, while the “College Grad With Debt” and “No College” samples both have a median age of 27.

Average down payment savings and estimated years needed to save a 20 percent down payment are based on data from only those respondents who stated that they plan to purchase a home in the future. Survey responses to questions on down payment savings are stated in ranges (e.g. “$100 to $199”). Point estimates are taken as the midpoint of the range, and the reported aggregate figures represent a straight average of these midpoints.

As a proxy for starter home prices, we use data on median condo prices from the National Association of Realtors. We estimate the number of years needed to save 20 percent of that price based on current saving levels and monthly saving rates. For simplicity, we assumed that home prices will increase at the historical average growth rate for the past 20 years. We make a similar assumption for wage increases, and assume that as their incomes grow, renters will continue put the same percentage toward down payment savings, although we do not account for increases in wages due to experience gained. Finally, we assume that renters will earn a return on their savings equal to the average growth of the S&P 500 over the past 20 years. National estimates use the national median condo price for all respondents, while metro level estimates use prices specific to each market.

- We stopped short of projecting wage growth along the people’s career progression, as we did not anticipate it could take decades to save for a down payment.↩

Share this Article