Explore strategies to find apartments that accept bankruptcies, and get tips to enhance your rental application. Start your search today!

Renting an apartment after bankruptcy can feel daunting, but with the right information and effort, it’s possible to get approved for a rental property. Start by looking for bankruptcy-friendly (or “second-chance”) apartments—rentals that accept applicants that have a bankruptcy in their credit history—and prioritize searching for privately owned apartments versus large property management companies. Consider also searching for properties in suburban areas with lower demand for rentals for the best likelihood of getting approved.

Rental approval usually depends on showing financial stability and reliability. Some landlords also prefer to rent to applicants who are 1–2 years post-bankruptcy.

To rent after bankruptcy, prepare to explain your situation, gather important documents (credit history, pay stubs, tax forms, bank statements, landlord and employee references) and consider finding a co-signer or guarantor.

We break down everything you need to know about how to find an apartment after a bankruptcy below.

Apartments That Accept Bankruptcies

What Are Bankruptcy-Friendly Apartments?

Bankruptcy-friendly (or second-chance) apartments are rentals that allow people with bankruptcies on their credit reports to apply. These are typically apartments owned by private landlords. They can be in high-demand cities or low-demand suburban areas, but applicants with bankruptcies will typically have more luck in areas with less renter competition and lower rental demand.

These apartments usually require additional documentation (a written explanation of the bankruptcy, credit history, pay stubs, tax returns, bank statements, landlord and employee references) and may not accept applicants until 1–2 years after the bankruptcy was filed.

How Does Bankruptcy Affect Your Ability to Rent an Apartment?

When landlords review applications, they typically look at:

Credit history (bankruptcies, late payments, collections)

Income verification (pay stubs, W-2s, bank statements)

A bankruptcy may raise red flags, but you can offset those concerns by showing financial recovery and reliability since your filing.

Keep in mind:

Some landlords won’t rent to anyone with a recent bankruptcy (within 1–2 years).

Bankruptcies remain on your credit history for 7–10 years, but their impact decreases over time, especially if you’ve rebuilt you’re credit and can prove a reliable payment history.

How to Find Apartments That Accept Bankruptcies

Most landlords will not advertise that they accept applications from renters with bankruptcy history, but those landlords do exist. Here’s how to find them.

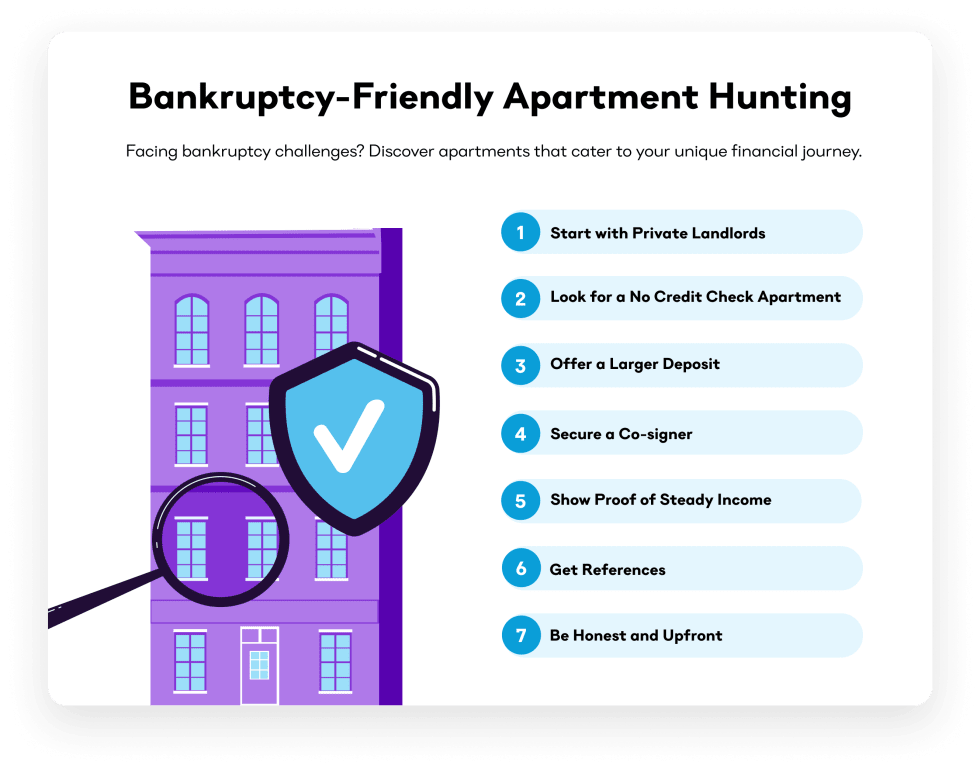

1. Focus On Private Landlords

Private owners are often more flexible than big management companies. They may be open to hearing your story and working with you if you can demonstrate reliability. Start with smaller buildings, duplexes, or single-family rentals. You can also check out our guide to no-credit-check apartments.

2. Expand Your Search Area

High-demand urban apartments are often stricter and more competitive. In suburban or less competitive markets, landlords may be more flexible and willing to work with applicants with complex circumstances.

How to Apply for Apartments Post-Bankruptcy

1. Prepare a Letter of Explanation

Landlords will see your bankruptcy on your credit report, so be upfront about it and reframe it as a turning point. Explain what led to it (job loss, medical bills, divorce, a death in the family, a business loss) and how you are rebuilding your finances. Back up your explanation with verifiable proof (see Step 2 below).

Copy and paste the template below to explain your bankruptcy:

[Your Name]

[Address]

[Phone Number]

[Date]

Dear [Prospective Landlord],

I would like to provide an explanation of my bankruptcy filing on [date] and give you more financial background to support my rental application.

My bankruptcy was the result of [life event / financial circumstance]. Since my filing, these are the steps I have taken to rebuild my finances:

[State your employment status and list your monthly / annual income: List the steps you have taken to rebuild your credit (for example, paying bills on time, using a secured credit card, using a rent reporting service, keeping credit card use under 30% of total credit).]

Additionally, I have savings of __, can pay a larger deposit of _ /_ upfront, have a guarantor / co-signer __, and __ [list any other supporting factors].

Thank you for considering my rental application. All of the relevant documents are attached.

Sincerely,

Your Name

2. Show Proof of Financial Stability

Your current ability to pay rent is one of the most important factors in any rental application. Most landlords expect tenants to have a monthly income of 3x the rent (called the 3x rent rule). Example: If your rent is $1,000/month, you’ll be expected to have a monthly income of at least $3,000.

Print out this checklist to help you organize your supporting documents:

Reference letters from past employers and landlords

A copy of your Letter of Explanation

3. Offer a Larger Deposit or Prepaid Rent

A larger security deposit (or paying 2–3 months of rent upfront) reassures landlords that you’re committed and financially capable. Be sure to confirm your state’s laws on maximum deposits. Prepaid rent is paying rent for a certain period upfront to give your landlord additional confidence in your application.

4. Secure a Co-signer or Guarantor

If a trusted friend or relative with good credit cosigns, it reduces the landlord’s risk. Guarantor services are also available for a fee in many cities.

Check out our Guarantor vs. Cosigner guide to get a better understanding of the differences.

What to Do If You’re Denied an Apartment After Bankruptcy

If you're denied an apartment due to bankruptcy, don't be disheartened. Start by asking the landlord or property manager for a reason in writing, as this can provide clarity for your future applications. Next, consider finding a co-signer or offering a larger deposit as an act of good faith. Continue your search, focusing on private landlords or specialized platforms that cater to individuals with financial challenges.

How Bankruptcy Affects Your Credit Score

The exact impact of bankruptcy on credit varies based on your individual credit history, but in general bankruptcy can reduce credit scores by 200 points or more.

How Long Does Bankruptcy Stay on Your Credit Report?

Bankruptcy stays on your credit report for 7–10 years, depending on the type of bankruptcy filed, but its negative impact on your credit score can diminish after 12–18 months, especially if you’re actively working to improve your credit. How long a bankruptcy stays on your credit report largely depends on the type of bankruptcy you've filed:

Bankruptcy Filing

Time on Credit Report

Best Landlord Type

Best Region

Chapter 7

10 years

Private

Suburban or Cities with Lower Rental Demand

Chapter 13

7 years

Private

Suburban or Cities with Lower Rental Demand

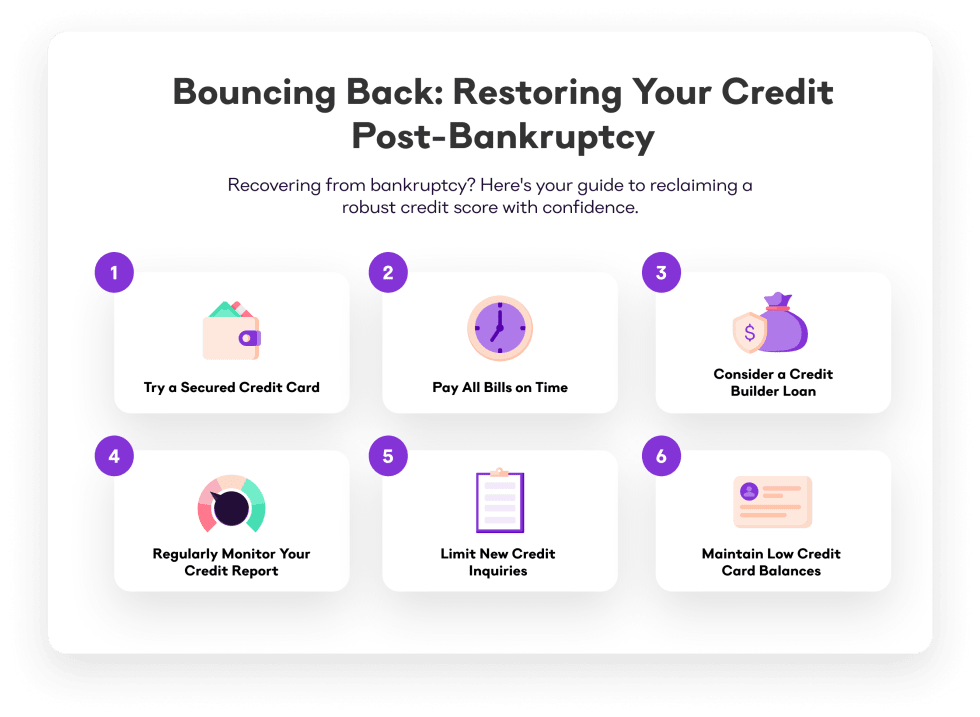

How to Rebuild Your Credit After Bankruptcy

With consistent effort, many renters see noticeable improvement in their credit scores within 6–12 months.

Activity

Impact

Pay bills on time

Payment history is one of the biggest factors in a credit score.

Open a secured credit card

Requires a deposit, easier to qualify for, helps build history.

Use rent reporting services

These services report timely rent payments to credit bureaus so your efforts are tracked.

Soft inquiries (background checks and preapprovals) lower your score by fewer points than hard inquiries (loans and rental applications).

Questions to Ask When Applying After Bankruptcy

Here are the main questions to ask a prospective landlord when applying for an apartment after filing a Chapter 7 or Chapter 13 bankruptcy:

Do you require a higher security deposit?

Will I need a cosigner or guarantor?

What type of credit check do you perform (soft vs. hard)?

Are there specific income or reference requirements?

What supplemental documents would you like to see in my application?

.

FAQs about Apartments that Accept Bankruptcies

What is a bankruptcy?

Bankruptcy is a legal process that allows individuals or businesses to reduce or eliminate debts they cannot pay. Under court supervision, debt may be discharged (Chapter 7) or repaid through a structured plan (Chapter 13). While it offers financial relief, bankruptcy remains on your credit report for 7–10 years, which landlords often consider during rental applications.

What is the difference between a bankruptcy and a foreclosure?

Bankruptcy covers multiple types of debt, including credit cards, loans, and medical bills, while foreclosure is specific to mortgages and occurs when a lender reclaims a property due to missed payments. A renter may file bankruptcy without ever going through foreclosure. However, both negatively affect credit scores and can make landlords cautious when reviewing rental applications.

Do I need to wait until my bankruptcy is discharged to start looking for an apartment?

While it might be easier to secure an apartment after your bankruptcy is discharged, some landlords or property management companies may be willing to rent to you before the discharge, especially if you can provide evidence of a steady income or other positive financial behaviors. It's crucial, however, to be transparent about your situation during the application process.

Is bankruptcy discrimination illegal?

In the United States, it is not illegal for landlords to deny applicants housing based on their bankruptcy filing history. However, there are some important exceptions to this rule.

Federal Law:

The Bankruptcy Code does not explicitly prohibit private landlords from discriminating against applicants based on their bankruptcy filing history. However, the Fair Housing Act (FHA) does prohibit private landlords from discriminating against applicants based on certain protected characteristics, such as race, color, religion, national origin, sex, familial status, and disability. In some cases, a landlord's decision to deny housing to an applicant based on their bankruptcy filing history could be considered a form of disparate impact discrimination under the FHA.

State and Local Laws:

Some states and municipalities have their own laws that prohibit private landlords from discriminating against applicants based on their bankruptcy filing history. For example, California's Fair Housing and Employment Act (FEHA) prohibits private landlords from denying housing to applicants based on their bankruptcy filing history if the applicant can demonstrate that they are capable of paying rent and complying with the terms of the lease.

According to the U.S. Department of Housing and Urban Development, public housing agencies can not discriminate against applicants or deny their applications solely based on a previous bankruptcy filing.

The content in this section is for informational purposes and does not serve as legal advice. Current state, local, and federal laws, as well as legislation regarding landlord and tenant protections, must be consulted and may change over time.

Can renting after bankruptcy help rebuild credit?

Yes, renting after bankruptcy, and paying rent on time, can help rebuild credit scores. Many landlords and rent-reporting services now share on-time rent payments with credit bureaus. Consistently paying rent in full and on time can improve your score, helping offset the impact of bankruptcy over time.

How long after bankruptcy can I qualify for an apartment?

You do not have to wait after filing bankruptcy to apply for an apartment, but some landlords may favor applications that are 1–2 years post bankruptcy.

How do I find rental properties that accept bankruptcies near me?

Search for private landlords rather than large property management companies by consulting local listservs and using our apartment match quiz.

Can I rent an apartment after bankruptcy?

Yes, but be prepared to provide proof that you are rebuilding your finances and your credit. You can legally rent an apartment after a Chapter 7 or Chapter 13 bankruptcy, depending on the landlord, region, and your complete financial picture.

What if I'm self-employed?

People who are self-employed and who have filed for bankruptcy in the past should provide supplemental income statements (1040s, contracts, profit & loss sheets, and bank statements) as part of their rental applications and include relevant details about their employment in their Letter of Explanation.

What is the difference between soft vs. hard credit inquiries?

Soft inquiries include background checks and preapprovals, while hard inquiries include loan and rental applications. Soft inquiries have less of a negative impact on your credit score (reducing it by fewer points) than hard inquiries. Always inquire about the nature of the credit inquiry during a financial application, so you can understand its potential impact on your credit score.

Dr. Katherine Blake is a content editor with Apartment List, where she helps ensure our renter and rental management content is fresh and informed by the latest data. Read More

Tristian Brown is a Senior Content Marketing Associate at Apartment List, where he manages high-quality content that helps modern renters find the perfect home. He brings an immense wealth of knowledge to the team, having earned a Bachelor of Arts in Marketing and European Management from the University of San Diego and EM Strasbourg Business School. Read More