Where New Supply Is (And Isn’t) a Problem – And What to Do About It

Multifamily operators today are potentially living within two very different realities. Some metros, like those in the Sun Belt, are battling oversupply and slowing demand, with concessions and longer lease-up timelines becoming the norm. Meanwhile, coastal and core markets are regaining pricing power as years of underbuilding collide with renewed demand.

Renters know they have options and they’re using that leverage to shop around. Misreading local supply conditions can mean softer rents, stalled absorption, costly concessions, and painful course corrections.

This post breaks down where new supply is being absorbed, where it’s dragging down rent growth, and, most importantly, how multifamily operators can tailor pricing, promotions, and placement strategies to the realities on the ground.

Supply Reality: Local Conditions Matter Most

The true supply picture is a patchwork of very different conditions and knowing which side of the supply divide your market is on is the difference between outperforming and playing catch-up.

Sun Belt: Oversupply from Pandemic-Era Building

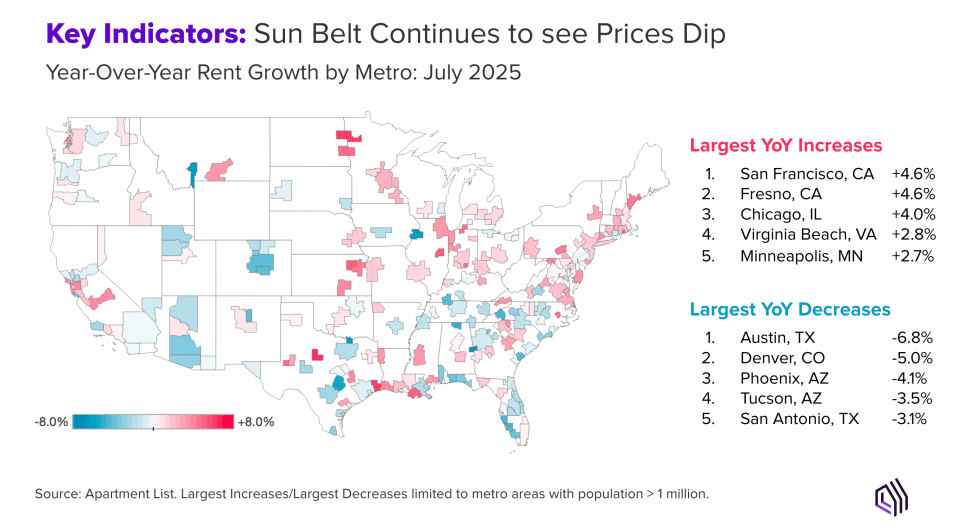

Markets like Austin (–6.8%), Denver (–5.0%), Phoenix (–4.1%), and Tucson (–3.5%) continue to post year-over-year declines. Each illustrates a slightly different absorption challenge:

- Austin: Added more than 25,000 units in 2023 alone (roughly 8% of its total stock), just as tech layoffs and slowing job growth undercut demand. Absorption rates in some submarkets have been running 40% below deliveries.

- Denver: Oversupply is concentrated in suburban corridors betting on migration that never materialized. Downtown assets are stable, but outlying properties are competing for a smaller pool of renters.

- Phoenix: Rents surged so quickly in 2021–22 that affordability ceilings were breached. Today, renters compare new multifamily units against single-family rentals at similar monthly payments, slowing absorption further.

The thread across these metros: deliveries are outpacing absorption. Vacancy is rising, concessions are common, and list-to-lease times stretch past 30–35 days.

Coastal & Core: Renewed Demand Meets Limited Supply

Contrast that with metros like San Francisco (+4.6%), Fresno (+4.6%), and Chicago (+4.0%), which are seeing rents climb.

- San Francisco: Years of underbuilding and restrictive permitting have left vacancy at just 3.5%. As AI-driven job growth and return-to-office policies kick in, renters are competing for a limited number of units, pushing pricing power back into operator hands.

- Chicago: Growth here reflects what economists call “relative affordability arbitrage.” Both renters and employers priced out of coastal hubs are finding stability in Chicago’s diverse, comparatively affordable market.

- Fresno: Benefiting from its position as a value alternative in the Central Valley, attracting renters priced out of Bay Area-adjacent markets, while construction pipelines remain constrained.

National averages set the context, but the strategy has to come from what your own submarket is signaling.

Reading the Supply Signals in Your Market

Permits and pipeline reports can help you see what’s coming 18 months down the road, but the decisions you’re making today depend on what’s happening in real time.

Absorption vs. Deliveries: The Critical First Signal

When deliveries consistently outpace absorption, vacancy rises quickly. That’s the story behind today’s 7.1% national vacancy rate.

Operators should be monitoring absorption monthly, not just annually. A useful rule of thumb: if fewer than 70% of new units are leasing within the first quarter after delivery, expect pressure on occupancy and effective rents.

Renter Behavior: A Leading Indicator of Supply Pressure

List-to-lease timelines averaged 28 days in July. Pair that with 54% of renters browsing without a firm move-in date, and you can see how abundant supply is shifting leverage back to the renter.

Budget flexibility offers another signal. 43% of renters ultimately lease above their stated budget, by a median of $220 per month, but only for properties that meet their lifestyle needs. That means “price sensitivity” is about perceived value and affordability. If renters aren’t willing to stretch, it may be a positioning issue as much as a pricing one.

Competitive Intelligence: The Operator’s Checklist

Your market intelligence should extend beyond vacancy reports. A weekly check can give you a sharper edge:

- Deliveries within a 3-mile radius, by quarter: to spot when new competition will hit. - Competitor concessions: not just the offer, but the gap between gross and effective rent.

- Tour-to-lease conversion rates: falling ratios are an early warning of oversupply.

- Renewal rates: declining renewals often indicate that new supply is pulling demand.

- Response times: renters may shop casually, but when they engage, they expect immediacy.

Market Classification: Defensive, Balanced, or Growth

Ultimately, the value of these signals is how they help you classify your market and choose the right strategy:

- High-Supply Pressure (Defensive): Long lease-ups, heavy concessions, list-to-lease above 35 days.

- Balanced (Optimize): Steady occupancy with list-to-lease in the 25–30 day range.

- Supply-Constrained (Growth): Vacancy tightening, list-to-lease under 25 days, limited concessions.

The local absorption story told through renter behavior and competitive dynamics will point your way forward.

Strategic Playbooks: Tailored to Market Type

1. High-Supply Pressure Markets: Play Defense with Precision

Characteristics: Oversupply, rising vacancy, list-to-lease often >35 days, concessions trending upward. Seen now in Sun Belt metros and suburban corridors.

Pricing Strategy:

- Focus on effective rent optimization rather than headline gross rents. A unit at $1,800 with one month free ($1,650 effective) can often outperform a $1,700 flat offer.

- Front-load concessions where possible. Renters perceive more value in upfront savings than in modest monthly discounts.

- Test renewal incentives before leaning too heavily on new lease concessions, turnover costs can climb quickly when you factor in vacancy, marketing, and downtime.

Operational Tactics:

- Response speed is currency. Renters may browse casually, but when they engage, they expect immediate follow-up.

- Highlight practical amenities: in-unit laundry, parking, storage. Renters will compromise on pickleball courts, not on basics.

- Start renewal conversations 120 days out. In competitive markets, renters compare options early.

Performance Marker: Try to hold occupancy above 93% and renewal rates above 60%, even if rent growth remains muted.

2. Balanced Markets: Optimize for Consistency

Characteristics: List-to-lease in the 25–30 day range, modest vacancy, limited concessions. The most common metro profile today.

Pricing Strategy:

- Test selective increases on premium units (top floors, best views, renovated finishes) while holding base pricing steady.

- Time concessions to lease expiration patterns. Offering incentives on spring renewals can smooth out heavy summer turnover.

- Adjust pricing every 3–4 weeks to stay in sync with shifting absorption, not just monthly.

Operational Tactics:

- Invest in process efficiency: shaving five days off an average 30-day lease-up cycle creates meaningful performance lift.

- Enhance digital renter experience (virtual tours, online applications, e-signatures). Renters have more time to shop, so ease of engagement matters.

- Begin renewal outreach 90 days in advance, framing renewals as convenience and certainty.

Performance Marker: Steady rent growth in the 1–3% range paired with smoother lease-up cycles and efficiency gains.

3. Supply-Constrained Markets: Lean Into Growth

Characteristics: Low vacancy (<4%), list-to-lease <25 days, minimal concessions. Coastal cores and select urban markets.

Pricing Strategy:

- Test rent ceilings with A/B pricing. In tight markets, pricing elasticity is best discovered in real time.

- Keep concessions minimal — in these conditions, they’re often unnecessary.

- Leverage budget flexibility. Remember: 43% of renters go over their stated budget by ~$220/month if the fit is right.

Operational Tactics:

- Streamline leasing processes to beat the 28-day national average. In high-demand markets, friction costs you.

- Implement waitlist management for premium units, think of it not just as a revenue strategy, but as market intelligence.

- Prioritize retention. Renters who stay extend pricing power and stabilize future performance.

Performance Marker: Rent growth above 4%, faster lease-ups, and stronger renewal capture that compounds over time.

90-Day Framework: Turning Strategy into Action

Once you’ve identified where your market is on the supply spectrum, it’s time to act on it. Here’s a simple framework to guide your next three months.

Weeks 1 & 2: Market Assessment

- Classify your market using the indicators outlined earlier: list-to-lease times, vacancy trends, concession patterns, and absorption vs. deliveries.

- Map the competition. Look at what’s happening within a 3-mile radius: how many units are being delivered, what incentives are on the table, and how competitors are positioning their properties.

- Benchmark renter signals. Compare your current list-to-lease time against the 28-day national average. Track tour-to-lease conversion and renewal inquiry timing.

Weeks 3 & 4: Test and Adjust

- Choose one playbook tactic that matches your market type, e.g., a renewal incentive in an oversupplied metro, or a pricing test on premium units in a supply-constrained market.

- Refine your leasing response workflows. Fast follow-up is increasingly the difference-maker, even with renters who start casually.

- Track renter engagement. Monitor application urgency (same-day vs. multi-week) to see whether you’re gaining momentum.

Month 2: Optimize What Works

- Review early results from your tests. Are shorter lease-up cycles showing up? Are renewal conversations yielding commitments earlier?

- Expand winning approaches: apply them across more units or properties.

- Adjust concessions strategically; front-load them where absorption is slow, or taper them off in markets showing stronger demand.

Month 3: Systematize and Scale

- Document your processes. Build playbooks into team routines so they don’t depend on one-off efforts.

- Train leasing teams on responding faster, positioning amenities effectively, and engaging residents earlier in the renewal cycle.

- Plan for seasonality shifts. With peak leasing now arriving in spring, smoothing demand through the fall and winter will protect performance heading into 2026.

Key Takeaway: Performance gains in today’s market come from small, well-timed adjustments that align with your market’s specific supply story. By treating the next 90 days as a testing ground, you can set yourself up to build repeatable systems that keep working as conditions evolve.

2026 Outlook: Positioning for the Rebound

The Pipeline Reality

- Deliveries remain elevated in 2025, keeping vacancy pressure high in oversupplied metros.

- Starts are declining, setting the stage for tighter supply-demand balance as completions taper.

- Geographic concentration matters. Sun Belt metros that built the most will continue to feel pressure, while many coastal and core markets are already showing demand resilience.

Positioning for the Rebound The operators who view today as a training ground will be best positioned when fundamentals improve:

- Sharpen leasing processes now. Faster response times, better renewal outreach, and consistent pricing discipline are habits that pay off when demand strengthens.

- Invest in renter experience. Renters have leverage today; keep them satisfied and you’ll retain them longer into the rebound.

- Stay data-driven. Submarket-level absorption and leasing signals will remain more predictive than broad averages.

Bottom line: 2025 may feel like a plateau, but 2026 is shaping up as an inflection point. By treating today’s soft spots as a proving ground, operators can ensure they’re ready to thrive when demand and supply rebalance.

Turning Market Complexity into Portfolio Performance with Apartment List

National averages may dominate the headlines, but they won’t guide your next lease signing or renewal. What matters most is how supply and demand are playing out in your submarket. Multifamily operators who read their local signals accurately will make smarter, faster moves than those waiting for national trends to catch up.

The fragmented landscape is a reality to be managed. Those who act decisively today will be the ones best positioned to capture tomorrow’s gains.

At Apartment List, we help you turn the signals we’ve discussed in this blog into stronger performance through our A-List Market, a performance-based leasing marketplace designed to deliver renters who are ready to sign and align your spend with results.

Get in touch with our team to learn how you can capture demand more efficiently in any supply cycle.