Apartment List's 2022 Millennial Homeownership Report

- According to the most recent Census data, the Millennial homeownership rate stands at 48.6 percent, more than 20 percentage points lower than the rate for Gen X and almost 30 percentage points lower than Baby Boomers.

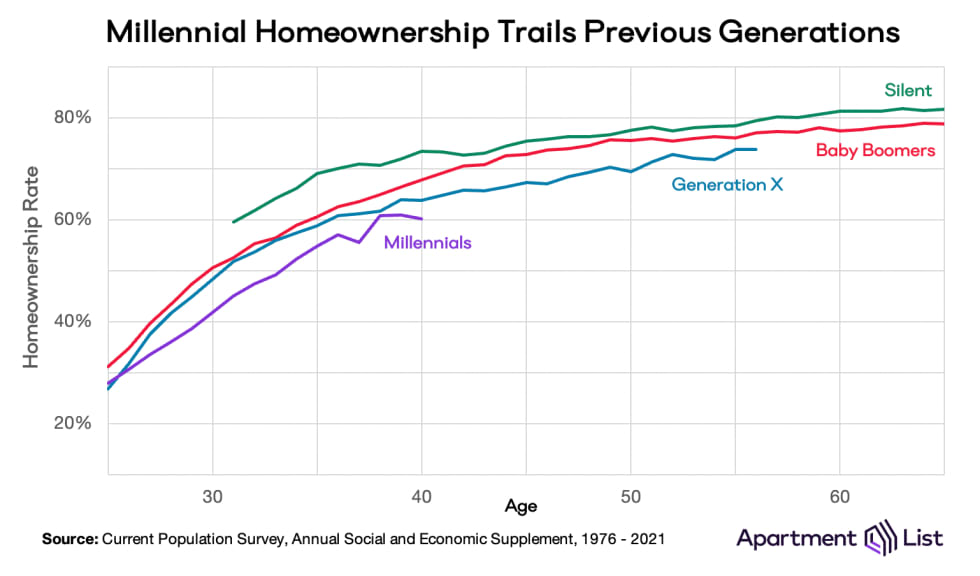

- Millennial homeownership lags even after adjusting for age. Among older Millennials who have hit age 40, 60 percent own homes. At that same point in life, 64 percent of Gen Xers, 68 percent of Baby Boomers and 73 percent of Silents owned homes.

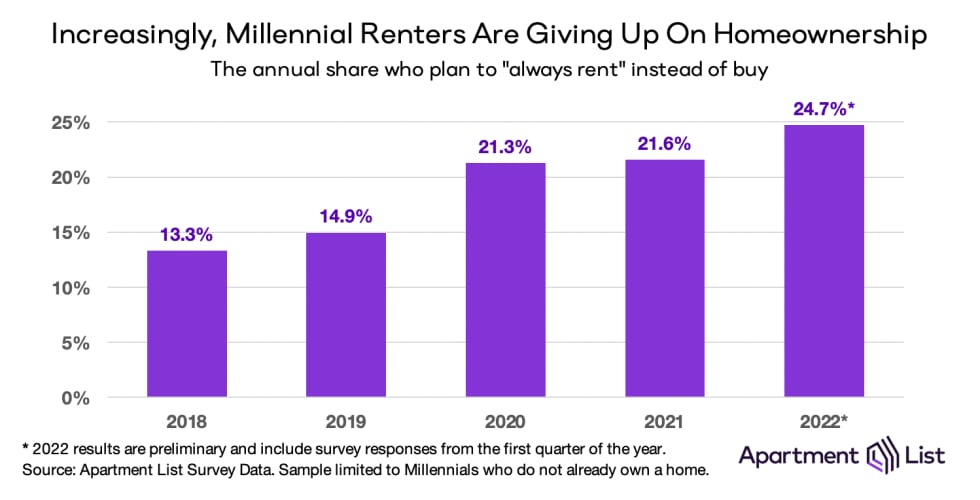

- With each passing year – and accelerated by the pandemic – an increasing share of Millennial renters say they will never own a home. 22 percent of Millennial renters view themselves as “always renters” in 2021, and preliminary data from 2022 shows that share increasing.

- As Millennials age, affordability becomes increasingly important to their housing choices. Other factors in the “rent or buy” decision (e.g., lifestyle flexibility) have become less important to Millennials as they age.

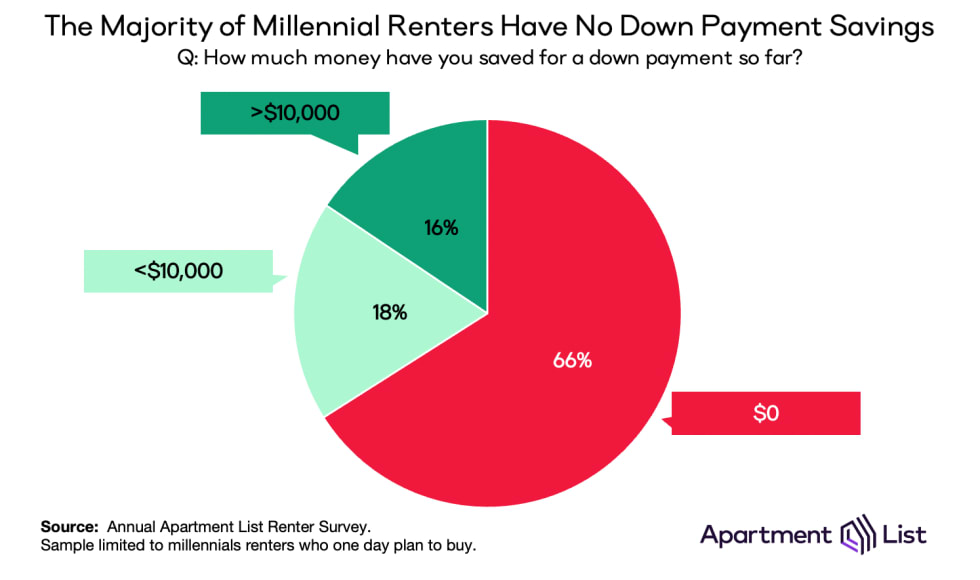

- Down payment savings rates remain shockingly low for Millennials who want to buy homes. In 2021, nearly two-thirds say they have no savings whatsoever, and only 16 percent have saved more than $10,000. The average savings of just over $12,000 represents just a 4 percent down payment on a median-priced condo today.

Emerging from the pandemic, Millennial homeownership continues to lag earlier generations

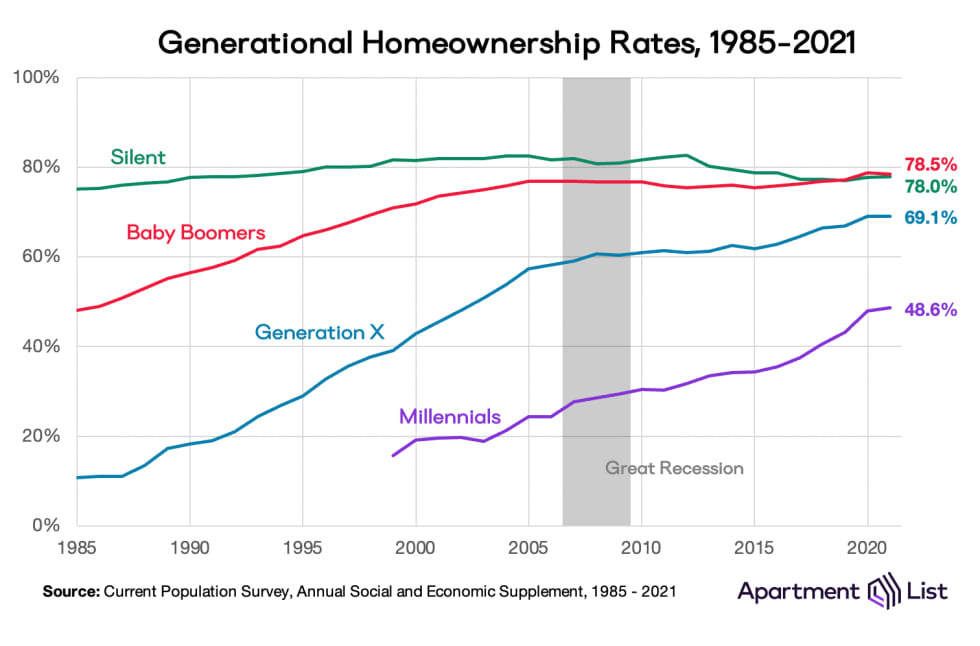

Millennials today are in their prime home-buying years (ages 25 to 40 in 2021, according to the definition we use here1) and as such, their homeownership rate has increased faster than any other generation over the past decade. In 2021 the millennial homeownership rate stood at 48.6 percent, up from 30 percent in 2011.2 But despite steady increases, the Millennial homeownership rate still significantly lags that of older generations. For Generation X (ages 41 to 56) the homeownership rate is over 20 percentage points higher than that of Millennials at 69.1 percent. Next is the Silent Generation (ages 76 and up), for whom homeownership has dipped recently but still stands at 78.0 percent. And finally, the nation’s highest homeownership rate belongs to the Baby Boomers (ages 57-75), who came of age after the post-WWII housing boom and today enjoy a homeownership rate of 78.5 percent.

It comes as no surprise that in 2021, Millennials in their 20s and 30s will have a lower homeownership rate than Boomers in their 50s and 60s. However, even when controlling for age, Millennial homeownership continues to trail previous generations. The chart below plots each generation’s homeownership rate by age to provide a more apples-to-apples comparison. Among the oldest batch of millennials who reached age 40 in 2021, the homeownership rate is 60 percent. In comparison, 64 percent of Gen Xers, 68 percent of Baby Boomers, and 73 percent of Silents owned homes when they were the same age. The gap emerges shortly after age 25 and persists throughout adulthood, highlighting how price increases and cultural shifts have led more Millennials to rent (or live with family) for longer.

Most recently, the COVID-19 pandemic sparked a housing market frenzy with polarizing effects for Millennial renters. On one hand, they purchased an outsized share of homes during the pandemic. Millennials account for 30 percent of adults but 43 percent of homebuyers during the pandemic, according to the National Association of Realtors.3 The Millennial homeownership rate rose more than 5 percentage points from 2019 to 2021, over twice as fast as any other generation.

On the other hand, housing supply dropped to all-time lows in late-2020 and prices soared. Across the country, the median home sales price jumped from $329,000 at the start of 2020 to $408,100 by the end of 2021. For Millennial renters who could not afford to buy a home before the pandemic, their opportunities for homeownership have waned dramatically over the two years that followed. Even more recently, mortgage rates have spiked above 5 percent for the first time in a decade, adding yet another hurdle for Millennials who have yet to attain homeownership.

Millennial renters are increasingly giving up on homeownership, and those who still plan to buy feel pressure to act fast

Our ongoing Apartment List renter survey has been monitoring home-buying sentiment among Millennials since 2018.4 Over the course of the pandemic, responses to our survey demonstrate two ways that Millennials are responding to an increasingly inaccessible housing market.

For one, a significant number of Millennial renters are bowing out from the increasingly-competitive housing market and expecting to forgo homeownership altogether. The share of “forever renters” increased modestly from 2018 to 2019 but saw a major jump once the pandemic rocked the housing market in 2020. Since then, more than 1-in-5 Millennial renters say they will never own a home, and in the first quarter of 2022 the share rises to nearly 1-in-4.

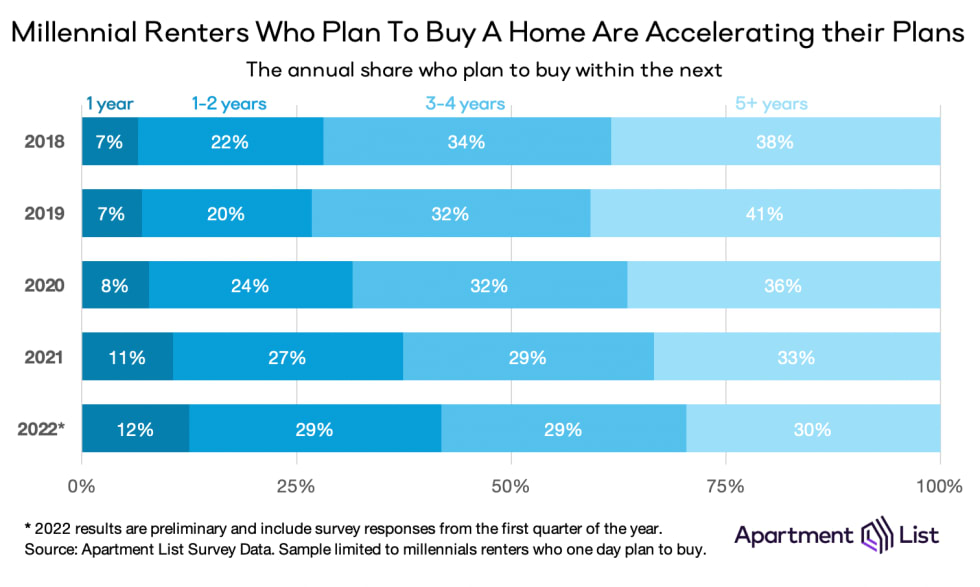

As for those who still plan to buy a home, the worsening affordability crisis is encouraging them to accelerate their timeline. In 2019, 27 percent of prospective Millennial homebuyers planned to buy within the following two years, but by 2021 that share jumped to 38 percent and in the first quarter of 2022 rose to 41 percent. This is consistent with broad generational sentiment that the housing market is only going to get more exclusive with time: more than 80 percent of Millennials believe that buying a home won’t be getting easier in the coming decade. Rising mortgage interest rates also encourage those who can afford to buy to do so promptly.

For a majority of Millennial renters, a lack of affordability is the only thing holding them back from homebuying

Renting offers certain lifestyle benefits over homeownership. Renters have more flexibility to move where and when they want, are free from the responsibilities (and unexpected costs) of homeownership, and can live in more amenity-rich communities than homeowners. The renter lifestyle fits nicely within the longstanding stereotype that Millennials value convenience and comfort over long-term commitments like homeownership. But our survey data suggests that these lifestyle benefits of renting are not the driving factor for Millennials who have yet to purchase homes. Millennial housing choices are predominantly rooted in financial stress rather than lifestyle flexibility. This applies to Millennial renters who plan to buy a home as well as those who do not.

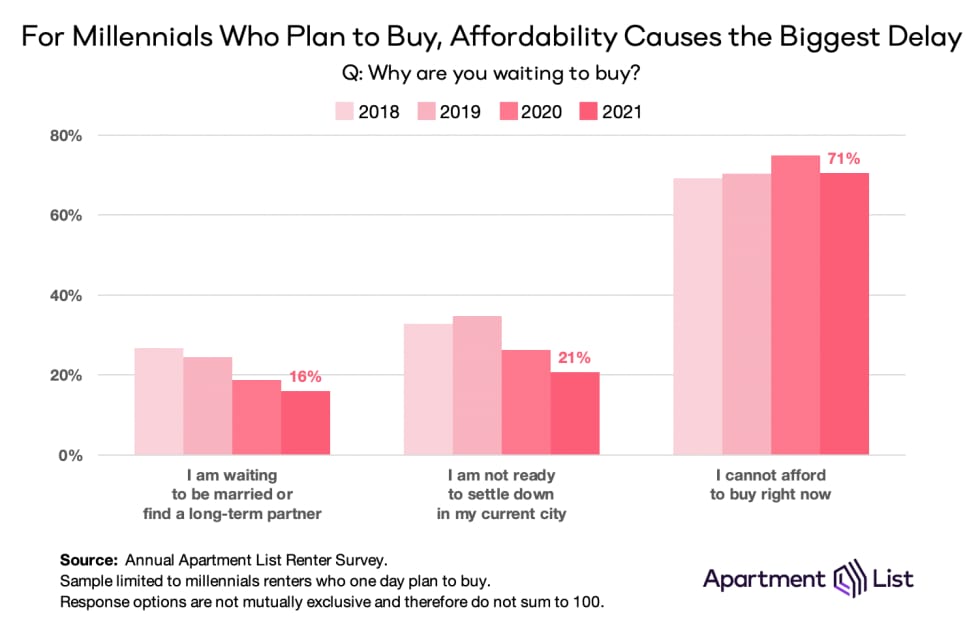

As Millennials enter their 30s and 40s, fewer say they are still waiting to settle down before buying a home. In 2021, just 16 percent say they are holding off to first settle down with a partner, and 21 percent are waiting to settle down in a specific city. Both factors have become less important over the past several years. Diminishing affordability, on the other hand, has caused the most widespread delays to Millennial homeownership. Over 70 percent say that they cannot afford to purchase a home, a worrying sign given the housing market has shown no signs of getting cheaper.

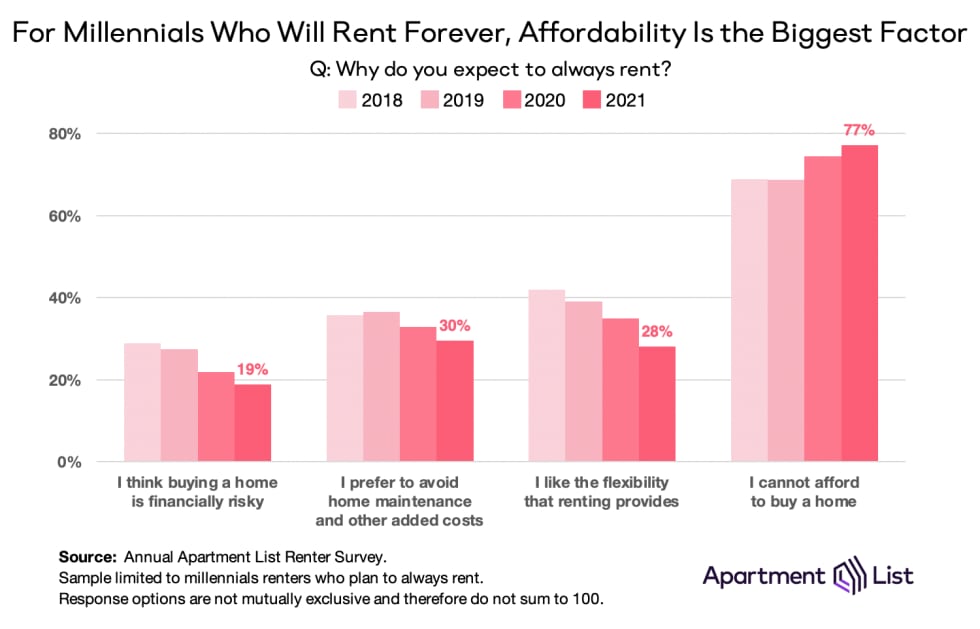

As for the millions of Millennials who plan to rent indefinitely, the primary reason is again affordability rather than lifestyle flexibility. Lifestyle benefits were a stronger factor pre-pandemic, but have become less important in recent years. So too has the burden of home maintenance and the notion that homeownership is a financially risky investment. Meanwhile, 69 percent of Millennials said a lack of affordability made homeownership unattainable in 2018 and 2019, but over the past two years that share has risen to over 77 percent.

Two-thirds of prospective Millennial homebuyers have zero down payment savings

Despite the fact that nearly 8 in 10 Millennial renters plan to buy a home in the future, many are still a long way from realizing their goal. Our survey finds that in 2021, 66 percent do not have any dedicated down payment savings, and only 16 percent have saved over $10,000. On average, Millennials with down payment savings have $12,773 set aside, representing just a 3 percent down payment on a median-priced house, or a 4 percent down payment on a median-priced condo.5 A traditional 20 percent down payment on that same condo would require $60,000 in savings. Only 2.3 percent of Millennial renters have that much saved.

To overcome a lack of personal savings, many Millennials turn to their parents for help. In 2021, 21 percent said they are expecting down payment assistance from family, highlighting how wealth in one generation can facilitate wealth in the next. But for the remaining 79 percent, homeownership may be realistic only if their personal savings increase dramatically and/or they narrow their search to the nation’s more affordable markets, which are becoming increasingly difficult to find.

What comes next

The COVID-19 pandemic has fanned the flames on the nation’s affordability crisis by triggering rapid price increases in both the rental and for-sale markets, not to mention broader inflation that has raised the cost of non-housing goods. Millennial renters who were priced out of homeownership before the pandemic face even greater barriers today, including rising mortgage interest rates. Millennials are the nation’s largest generation but have the lowest homeownership rate, creating pressure that trickles down into the rental market where an increasing number of families must compete for vacant apartments. Rents prices are up 17 percent since the start of the pandemic, and certain popular cities across the country have seen prices rise more than twice that fast.

Beyond Millennials, the pandemic has also been a defining economic moment for the following generation, Z. Currently ages 24 and younger, Gen Z renters have been thrust into a housing market that immediately jumped in price. The coming years will reveal how Gen Z fares compared to Millennials, but according to our renter survey already 20 percent already say they expect to rent forever - a similar share as the Millennial renters one decade older.

One remaining opportunity for both generations is the widespread adoption of remote work, which has established itself as a permanent fixture in the post-pandemic economy. Decentralized businesses offer their employees the unique opportunity to access high-paying jobs in lower-cost parts of the country. Previous research on the remote work revolution has uncovered that remote workers earn more, move more, and often relocate to more-affordable housing markets. While some workers - especially younger ones - have reservations about working from home, it may offer the best opportunity for those who value homeownership.

- Throughout this report, our generation definitions are consistent with the Pew Research Center. The Millennial generation was born 1981-1996, Generation X was born 1965-1980, the Baby Boomer generation was born between 1946-1964, and the Silent generation was born 1928-1945. ↩

- Source: Current Population Survey (CPS) Annual Social and Economic Supplement (ASEC), accessed via IPUMS-CPS. The Millennial homeownership rate is defined as the percentage of Millennial-headed households in the United States that are owner-occupied.↩

- Source: National Association of REALTORS Research Group: 2022 Home Buyers & Sellers Generational Trends Report. Note that NAR defines Millennials as being born between 1980 and 1998, a wider definition than used by Pew and this Apartment List report. ↩

- Our Apartment List renter survey has collected responses from more than 31,000 Millennials since 2018. It is not a panel survey, and in each year the pool of respondents contains only renters who have not purchased a home.↩

- The median sales price for a house in 2021 Q4 is $408,100 according to the Federal Reserve Bank of St. Louis (source). The median sales price for a condo in 2021 Q4 is $299,900 according to the National Association of Realtors (source).↩

Share this Article