How will remote work impact housing location preferences?

Overview

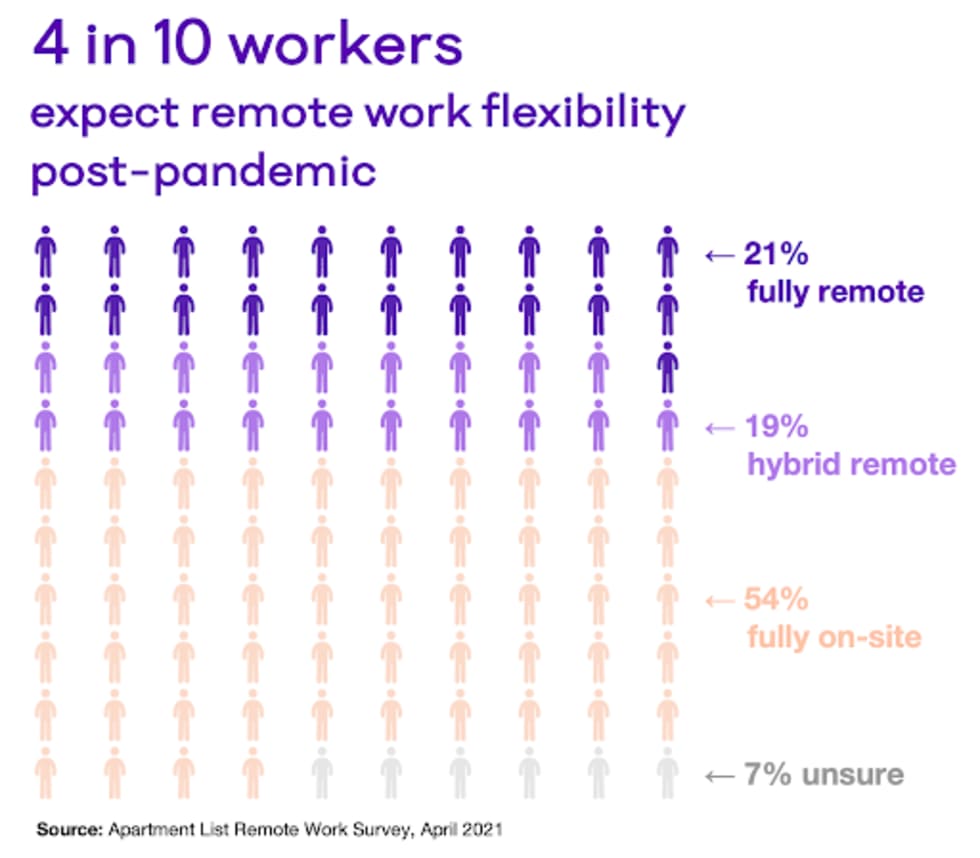

- In a survey of 5,000 employed adults across the U.S., we found that four-in-ten workers expect to have some form of continued remote work flexibility post-pandemic. 19 percent expect to have a hybrid arrangement that allows for remote work multiple days per week, while 21 percent expect that they’ll have the ability to work exclusively remotely.

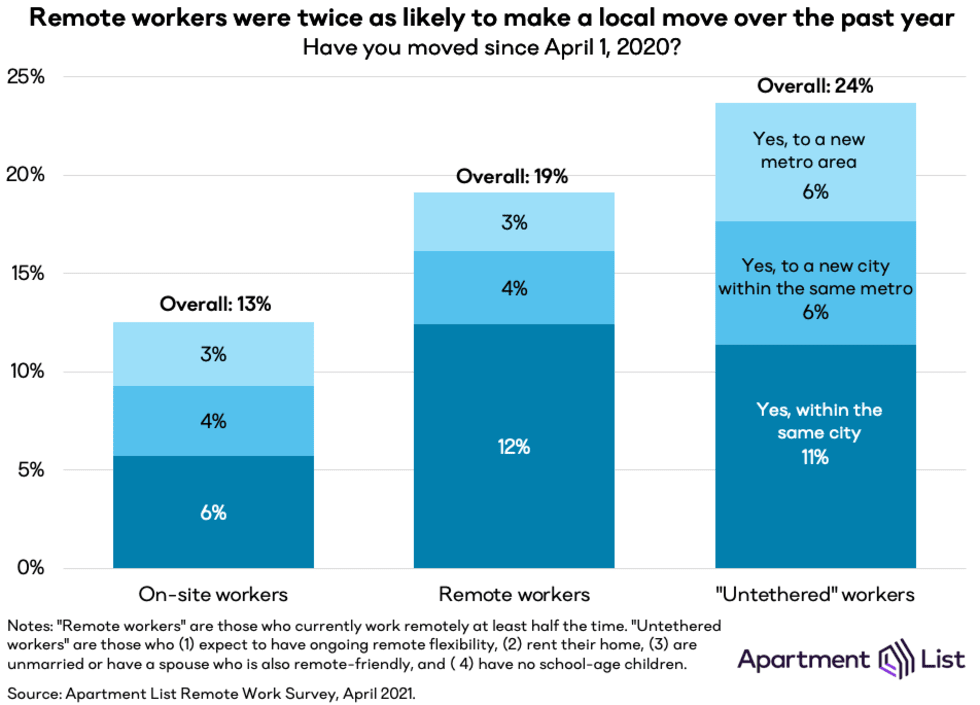

- Remote work is already spurring increased moving activity. 19 percent of remote workers moved over the past 12 months, compared to 13 percent of workers whose jobs require them to be on-site. However, most of these additional moves were local -- remote and on-site workers were equally likely to move to a new city or a new metro.

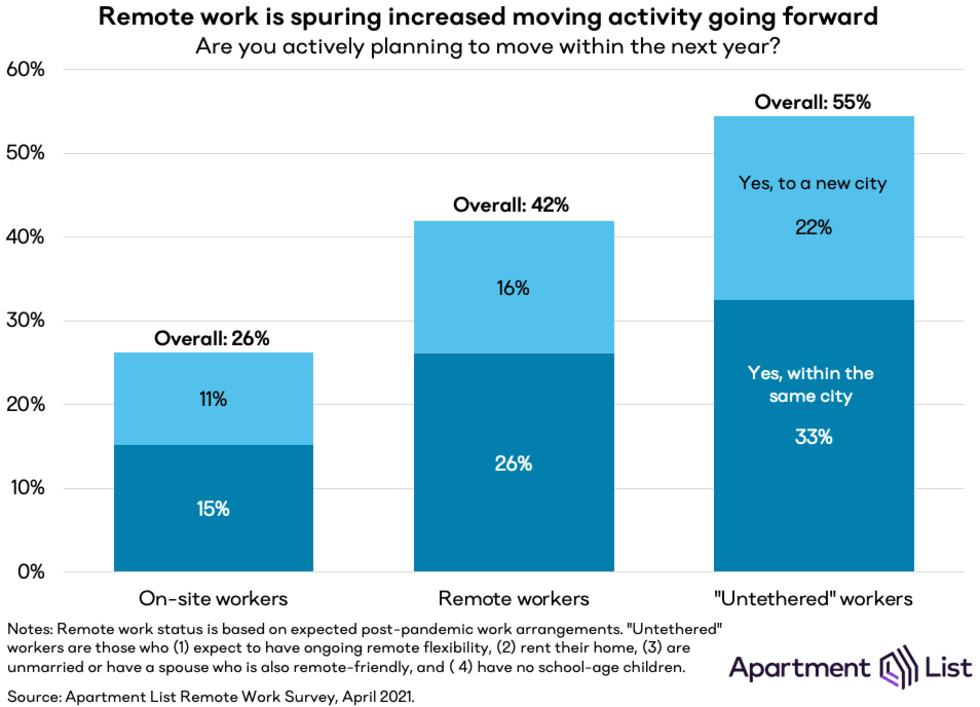

- Looking forward, 42 percent of remote workers say that they’re planning to move over the next 12 months, compared to 26 percent on-site workers. Remote workers are more likely to be planning local moves as well as moves to a new city.

- 35 percent of remote workers who are planning an upcoming move say that they plan to relocate to a more affordable market, more than double the rate for on-site workers, indicating that we may see an outflow of remote workers from the nation’s most expensive housing markets going forward. This finding also highlights the important equity implications of remote work -- on-site jobs are lower paid, on average, but on-site workers have less flexibility to relocate in search of more affordable housing.

- Overall, remote workers told us that the most important factors in their decision of where to live over the next several years are “access to a housing market where I can afford homeownership” and “access to natural amenities.”

- Our survey data also validates our earlier hypothesis that “untethered workers” -- remote workers who are also not tied down by homeownership or family obligations -- will represent the leading edge of remote work related migration trends. 23 percent of the untethered workers in our survey moved over the past year and 55 percent plan to move in the coming year, both well above the shares for remote workers overall.

Introduction

With vaccine eligibility now open to all adults nationwide, we’re fast approaching the day when COVID risk will no longer prevent work from being done in person. However, as we’ve stated in the past, the remote work revolution was well underway prior to the pandemic, and it is poised to continue after the threat of the virus has subsided. In a recent survey of 5,000 employed adults across the U.S.1, we found that just over half of respondents are currently working remotely at least half the time, and of those remote workers, more than 3-in-4 expect to have continued remote flexibility post-pandemic.

This unprecedented step change in how workplaces are organized is weakening the link between job choice and housing choice, and remote workers are already taking advantage of this newfound freedom to move at higher rates. Understanding the geographic preferences of this group is now more important than ever, as their migration trends will have the potential to disrupt housing markets across the country.

Our survey sheds new light on the factors that are motivating moves among remote workers and the attributes they value when choosing where to live. We find that the considerations of remote workers differ from those of on-site workers in important ways. These preferences will drive how remote work will impact the housing market over the next several years.

Remote workers moved more than on-site workers over the past year, but most moves were local

Overall, 16 percent of our survey respondents state that they have moved since last April. Among those who moved, more than half (57 percent) stayed within the same city where they had already been living, while 20 percent moved to a new metro and 12 percent crossed state lines. For comparison, data from the Census Bureau shows that from 2018 to 2019, just 9.8 percent of Americans moved to a new residence. Although the Census data is not directly comparable to our survey data, this disparity nonetheless indicates that the pandemic seems to have prompted more moves over the past year than would typically occur.2

Drilling down further into this data, we find that remote work flexibility was an important determinant of who moved last year. Among those who are currently working remotely, nearly one-in-five moved over the past 12 months, a rate that is 53 percent greater than the share for on-site workers.3 But while the prevailing narrative around remote work related migration has tended to focus on stories of remote workers making life-changing long-distance moves, we find that within our survey sample, the heightened moving activity among remote workers was almost entirely local. Over the past year, remote workers were twice as likely as on-site workers to move within the city where they had already been living, but the share that moved to a new city or metro was identical across the two groups.

Our survey also allows us to identify workers who are part of the “untethered class,” a concept which we defined in an earlier report. Untethered workers are employed in remote-friendly occupations, but also are not tied down by homeownership or family obligations.4 If given the opportunity for long-term remote work, the untethered class will face no significant barriers to moving wherever they please, and we have therefore hypothesized that this group will represent the leading edge of any new migration patterns spurred by remote work.

Results from our survey data validate that the untethered class is indeed a group with a high rate of geographic mobility. 24 percent of untethered workers in our survey moved over the past twelve months, notably higher than the rate for remote workers overall.5 The share of untethered workers who made a local move within the same city was in line with the rate for all remote workers, but untethered workers were more likely to make long-distance moves. 6 percent of untethered workers moved to a new metropolitan area over the past year, double the 3 percent share for the broader group of remote workers.

“More space” was the top motivator for pandemic moves, regardless of remote work status

Recent movers were also asked about the factors that motivated their decisions. Overall, the most common motivation was a desire for a more spacious home, a factor cited by about 30 percent of remote and on-site workers alike. But responses for the other factors we consider point to meaningful differences between remote and on-site workers. For example, 22 percent of remote workers say that they moved “to a location with great access to natural amenities,” compared to just 13 percent of on-site workers; this factor represents the biggest gap between the two groups. Remote workers were also significantly more likely to move to a more affordable market, to move someplace further from their job, or to make a temporary move to “wait out” the pandemic. The differences in these responses reflect the degree to which remote workers haven taken advantage of their newfound flexibility amid the pandemic.6

The responses of untethered workers (not shown in the chart above) again confirm that this group represents a distinct subset of remote workers. 26 percent of untethered workers who moved recently told us that they moved to a more affordable market, 25 percent moved to be closer to family, 21 percent moved to be closer to friends, and 16 percent made a temporary move. These shares are all higher than the comparable rates for remote workers as a whole.

4-in-10 workers expect to have continued remote flexibility post-pandemic

We have been hypothesizing for some time that a broad embrace of remote work would outlast the pandemic, but in the past, we have largely relied on plans announced by a handful of major companies as supporting evidence. But our new survey data provides an even stronger footing to support a bullish outlook for remote work. 51 percent of our survey respondents are currently working remotely at least half time, and 29 percent report that they perform their jobs exclusively remotely.

Looking forward, more than 3-in-4 of those who are currently working remote at least half time expect that they’ll have some version of remote flexibility going forward. 40 percent tell us that their employer has signalled that they will be allowed to work fully remotely post-pandemic, and an additional 37 percent expect to have a hybrid arrangement that allows for remote work multiple days per week. Just 10 percent say that their employer has signalled a full return to on-site work, while the remaining 13 percent are unsure of future work arrangements. Across the full sample, our survey implies that 40 percent of the overall workforce expects to have at least partial remote work flexibility post-pandemic, while 21 percent expect that they’ll have the ability to work from anywhere going forward.

Remote work is prompting moving plans and changing preferences

Such a broad embrace of remote work would be unprecedented, and it’s possible that some employers may reverse course and require more work to be done on-site. And given how anomalous the past year has been, it’s not obvious that the mobility patterns of remote workers amid the pandemic will be a good predictor of how they will behave in the future. Nonetheless, our data clearly show that a heightened rate of mobility among remote workers extends to forward-looking expectations.

Overall, 32 percent of respondents tell us that they’re actively planning to move within the coming year (19 percent within their current city and another 13 percent to a new city), but these figures vary significantly when comparing remote and on-site workers.7 Among those who expect to have remote flexibility going forward, 42% say that they’re planning to move within the next year, compared to just 26% of those who expect to be working mostly or fully on-site when the pandemic subsides. Remote workers are 72 percent more likely than on-site workers to be planning a move within their current city, and 42 percent more likely to be planning a move to a new city. Untethered workers are again the most mobile group -- more than half tell us that they plan to move within the next twelve months, and untethered workers are more than twice as likely than on-site workers to be planning moves both within their current cities and to new cities.

Remote workers are twice as likely to say that they’re planning to move to a more affordable housing market in the next 12 months

Among those planning an upcoming move within the next 12 months, we also asked them about the factors involved in their planned move, again in a “select all” format. Overall, the most frequently selected statements were “I plan to purchase a home” (49 percent) and “I plan to move to a more spacious home” (30 percent). For both factors, the shares were essentially identical for both on-site and remote workers. It seems that a historically tight inventory of for-sale homes is not discouraging the persistent goal of homeownership. And despite now needing to use their homes as workspaces, remote workers are no more likely than on-site workers to be looking for more space.

However, responses to this question were not equivalent for remote and on-site workers across the board. Most strikingly, 35 percent of those who expect to continue working remotely post-pandemic and who are planning an upcoming move tell us that they’re planning to relocate to a more affordable housing market. This is double the 17 percent rate for workers who expect to be working on-site post-pandemic.8 This finding suggests that we may see a continued net-outflow of remote workers away from the nation’s most expensive housing markets, such as San Francisco and New York City.

This result also illuminates the important equity implications of remote work. On-site workers earn less on average but don’t have the same flexibility to move to alleviate housing affordability issues. We know that remote-friendly occupations tend to be higher paid and that lower-income households struggle disproportionately with housing costs, yet the share of remote workers who say that they plan to lower their monthly housing costs with an upcoming move (28 percent) is higher than the share among on-site workers (25 percent). Those who can work remotely are being freed up to move to markets with more affordable housing, while the on-site workers who would benefit most from reduced housing costs lack that geographic flexibility.

In terms of the types of places that they would like to live, just 14 percent of remote workers who plan to move say that they are planning to move someplace with greater access to natural amenities, the same share as on-site workers. While remote workers were significantly more likely to move for natural amenities over the course of the past year, forward looking plans suggest that the influx of remote workers to “Zoom towns” such as Bozeman, MT may have been a temporary response to the unique circumstances of the past year, rather than the beginning of a long-term trend.9 Meanwhile, 16 percent of remote likely movers are planning to move someplace with greater access to urban amenities, five percentage points higher than the share among likely movers who work on-site.

Remote work’s impact on moving plans and preferences will play out gradually in the coming years

Because expectations about the next 12 months are likely still being impacted by the pandemic, we also ask about plans over a longer horizon, and continue to find an increased propensity to move among remote workers. 54 percent of those with expected remote flexibility say that they are at least somewhat likely to move over the next three years, compared to just 39 percent of those who expect to be working primarily on-site.10

When asked to consider if permanent remote flexibility would impact housing preference, there is a clear indication that it would, particularly among those who are most likely to actually move. 46 percent of all respondents say that their location preferences would change if they had full remote flexibility, but this share jumps to 63 percent among those who are at least somewhat likely to move within the next 3-years. Hybrid arrangements have a somewhat weaker reported effect on location preferences. Just 32 percent of respondents say that their location preferences would change in response to hybrid remote flexibility, but among those who are at least somewhat likely to move in the coming years, half answered yes to this question.

We then asked respondents to consider the most and least important factors in determining where they would want to live over the next several years. Among all respondents, 28 percent say that “access to family nearby” is the most important factor, followed by “access to a housing market where I can afford homeownership” at 19 percent. However, these priorities are flipped among those who are at least somewhat likely to move over the next three years -- 23 percent say that attaining homeownership is the most important factor, followed by family at 20 percent. This disparity is interesting to note given that the likely movers are the ones who will be driving migration patterns over the next several years.

When we break down these results between those who expect to have remote flexibility post-pandemic and those who expect to be working on-site, the ability to afford homeownership continues to rank number one for both groups, but compared to on-site workers, a smaller share of remote workers selected this factor. Remote workers were also less likely to cite “access to local job opportunities” as their most important factor (12 percent, compared to 15 percent for on-site) and a greater share selected it as the least important factor (16 percent vs 13 percent), confirming that attitudes among remote workers are reflecting the weakening link between job location and housing location.

Meanwhile, remote workers are more likely than on-site workers to place value on urban amenities, consistent with responses to earlier questions in our survey. Remote workers are also more likely to value proximity to their friends. Overall, responses were spread somewhat evenly across the six factors we consider, on both the “most important” and “least important” sides, showing that housing decisions are complex and multi-faceted. Remote workers are not a monolithic group, and the moves that they make in the coming years will reflect a range of sometimes competing priorities.

Conclusion

One-in-four American workers expect that they will continue to have either partial or complete remote work flexibility once the pandemic subsides. Compared to those who are required to work on-site, remote workers are significantly more likely to be planning a move over the next several years, and a majority tell us that remote flexibility will have an impact on their preferences of where to live.

When asked about the specific factors influencing their planned moves, housing affordability and the ability to attain homeownership emerge as key factors, implying that some of the nation’s most expensive housing markets could see an outflow of remote workers who are ready to purchase homes but can’t afford to do so in markets like San Francisco and New York City. Our survey also indicates that remote workers place high value on being close to family, indicating that some who are ready to settle down may move back to the places they grew up. And although many remote workers moved for nature during the pandemic, forward looking plans show that urban areas still have high appeal, and this is likely to grow as city-life begins to regain its vibrancy. This suggests that the places most likely to attract remote workers may be the ones that were already doing so pre-pandemic -- markets such as Austin and Nashville that offer the urban amenities that remote workers value, at a significantly lower cost than coastal superstar cities.

- Our survey was conducted from April 9-10, 2021 and administered in collaboration with SurveyMonkey. We collected responses from over 5,000 Americans who are currently employed full-time, and our sample is representative of the U.S. population along the dimensions of gender and age.↩

- Figures from Census are estimates for the entire U.S. population, while our survey was limited to adults who are employed full-time. While complete migration statistics for 2020 have not yet been released, data from the USPS reports 30 million change-of-address requests for 2020, which is equivalent to the total number of moves reported in the Census CPS for 2019; because not everyone who moves files a change-of-address request, this data point also supports the hypothesis that 2020 saw heightened moving activity.↩

- Remote workers are defined here as those who are currently working remotely at least half the time, while on-site workers are those who are working mostly or entirely on-site. The heightened propensity to move among remote workers is not simply driven by demographics. In a binomial regression controlling for age, income, homeownership status, and population density of current residence, we found that the ability to work remotely has a positive and statistically significant impact on the likelihood of moving over the past year.↩

- Specifically, we define untethered workers in our survey as those who meet the following criteria: (1) expect to have ongoing remote flexibility post-pandemic, (2) rent the home in which they live, (3) are unmarried or have a spouse who is either unemployed or also expects their job to be remote-friendly going forward, and (4) have no school-age children.↩

- It’s worth noting that in our definition of untethered workers, homeownership proves to be a much stronger tether than the family factors we consider. 22 percent of renters moved last year, compared to just 13 percent of homeowners. If we loosen our definition of untethered workers to allow homeowners, the share of untethered workers who moved last year falls from 23 percent to 19 percent. However, if we continue to restrict to renters, but loosen the constraint on family tethers, it actually increases to 25 percent.↩

- Remote workers were more likely than on-site workers to select nine of the ten statements we presented them with. Meanwhile, 17 percent of on-site workers said that none of these statements applied to their move, compared to just 6 percent of remote workers. This may imply that on-site workers were more likely to have moved out of necessity rather than to better align their housing with their preferences.↩

- These rates are far above normal mobility rates. While there is some reason to believe that we may see a spike in moving activity this year, it is also likely that some share of these planned moves will not actually occur. That said, comparing forward looking expectations across groups is still informative.↩

- Note that we observe a much smaller gap between the groups in the share who say that they’re planning to move further from their job, with just 16 percent of remote workers saying that this is a factor in their planned move. This fact may appear to contradict the high share that tell us that they plan to relocate to a new market, however it most likely reflects an issue in interpreting the wording of the survey question. If remote workers now consider their home to be their “job location,” they might not select this factor, even if they are moving further from their employer’s primary place of business.↩

- It’s worth noting that the share of respondents who tell us that they’re reversing a temporary move from the past year is lower than the share who say that they made temporary moves, suggesting that some moves which were intended to be temporary may end up being permanent.↩

- 65 percent of untethered workers are at least somewhat likely to move within the next 3 years, significantly higher than the share among expected remote workers as a whole↩

Share this Article