Homeownership Rates by Generation: How Do Millennials Stack Up?

- Millennials are the nation’s largest generation and a powerful force in the housing market, but their impact on the market is largely misunderstood. The goal of this report is to clarify misconceptions about millennial homeownership and provide historical context by comparing millennial behaviors to those of earlier generations.

- Today, 43 percent of millennial households own their homes. This homeownership rate sits well below other generations, but is growing the fastest. Millennial homeownership has increased steadily even through the aftermath of the Great Recession.

- Homeownership in general has been on the decline for at least the last three generations. After adjusting for age, millennials, gen Xers, and baby boomers have all purchased homes at a slower rate than the generation that preceded them.

- Millennials are often thought of as a generation of renters, but their homeownership rate is catching up to generation X. In the coming years, they may become the first generation since World War II to reverse the trend in declining homeownership.

- Several socioeconomic factors including income, education, and race have contributed to the broad decline in homeownership. For millennials particularly, lower homeownership rates are concentrated among African-Americans, those without a college education, and surprisingly, those with high incomes.

Introduction

In 2019 millennials outnumbered baby boomers for the first time, becoming the nation’s largest generation.1 As such, they are a powerful force in the housing market. Now in their prime home-buying years, millennials are stirring up discussions about their behaviors and preferences. The Great Recession interrupted homeownership plans for some and forced many millennials to rent longer, but what about since then? After a decade of economic recovery, the narrative about millennial homeownership has become surprisingly opaque.

Take for example the following headlines from major news outlets, all published in just the last year and a half. One says millennials “have officially entered the housing market”2 while another cautions “millennial home buyers might never come knocking.”3 One argues that a rise in national homeownership is “driven by younger buyers”4 while another calls them a “driving force behind declining homeownership across America.”5 One questions if millennials are “killing the U.S. housing market”6 while another claims they are “reviving the suburbs and exurbs.”7

The goal of this report is to cut through these competing narratives, to clarify exactly how millennials are faring in the market, and to compare millennial homeownership to that of previous generations. In doing so, we find that despite the trauma of the Great Recession, the millennial experience is not particularly unique. Rather, it is the continuation of a decades-long trend. Millennials are not the first generation to own fewer homes than the last; in fact, homeownership growth has been slowing since before they were born.

How do you define millennial homeownership?

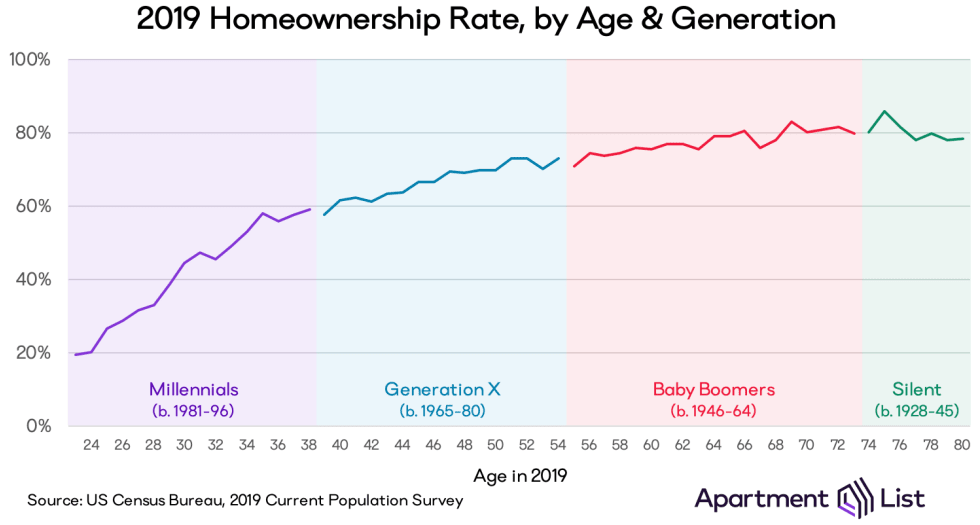

Millennial homeownership is conceptually simple but not universally defined. There is no central authority that determines when one generation ends and the next begins.8 For this report we adopt definitions from the Pew Research Center, one of the nation’s leading demographic think-tanks, which defines American generations based on shared attitudes, behaviors, and experiences. According to Pew, millennials were born between 1981 and 1996, putting them between the ages of 23 and 38 in 2019. Members of generation X were born between 1965 and 1980, baby boomers were born between 1946 and 1964, and those born before 1945 belong to the silent generation.

To determine the millennial homeownership rate, we identify all households headed by a millennial and calculate the percentage that are owner-occupied.9 A similar technique is used to derive homeownership rates for earlier generations. Plotting these rates across ages in 2019 shows the homeownership curve below, which traces a logical path.

Homeownership rises quickly as people buy their first homes in their 20s and 30s (a span currently occupied by millennials). It continues to rise, but at a slower rate, through their 40s, 50s, and 60s (today’s gen Xers and younger baby boomers). Finally it plateaus in their 70s (older baby boomers) and then actually starts to recede, as some senior citizens sell their homes and return to renting.

What is the millennial homeownership rate?

Today the millennial homeownership rate is 43 percent, well below the rates of generation X (67 percent) and the baby boomer and silent generations (77 percent). An important feature of millennial homeownership that often gets muddled in the media conversation is that it is increasing, and with few minor exceptions, it has always been increasing. The oldest millennials turned 18 in 1999, and every year since then there has been a net increase in the number of millennial-owned homes. Since the Great Recession, the millennial homeownership rate has grown faster than any other, particularly in the last five years while the economy has expanded quickly. Today, millennials are the least likely to own a home, but they are the most likely to purchase one.

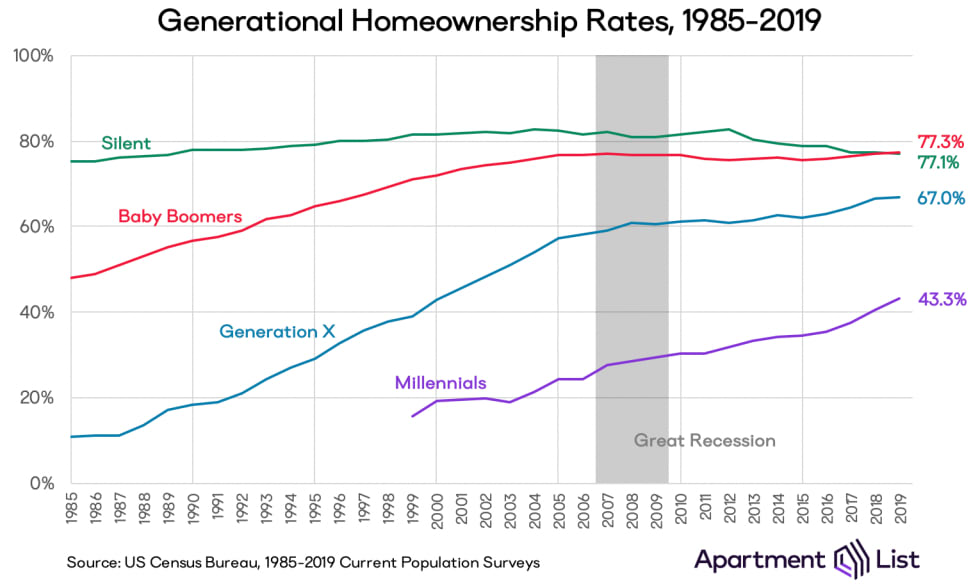

This chart shows the impact of the Great Recession on each generation’s homeownership rate. The silent, boomer, and X generations were all experiencing positive homeownership growth in the years leading up to 2007. But then the momentum stopped; from 2007 to 2016 silent generation homeownership dropped from 82 to 79 percent while boomer homeownership dipped slightly from 77 to 76 percent. Generation X homeownership, which grew 23 percentage points in the decade before the recession, grew just four in the decade after. Millennials were the only generation substantially improving their homeownership rate during this time of economic turbulence. While the national homeownership rate was shrinking to its lowest point in half a century, the millennial homeownership rate increased eight percentage points.

Comparing year-over-year homeownership rates has its advantages and disadvantages. On one hand, it show that the mid-2000s drop in homeownership was not just a story about millennials being unable to afford homes. It was also a story about generation X homeownership slowing dramatically and many older Americans losing their homes altogether.

On the other hand, this approach compares generations at different stages in life. It is not surprising that even during a recession, those in their 20s will buy homes faster than those in their 50s. The task is then to control for these differences in age and check if millennials are purchasing homes at a similar rate as older generations did when they were the same age.

How does millennial homeownership compare to previous generations?

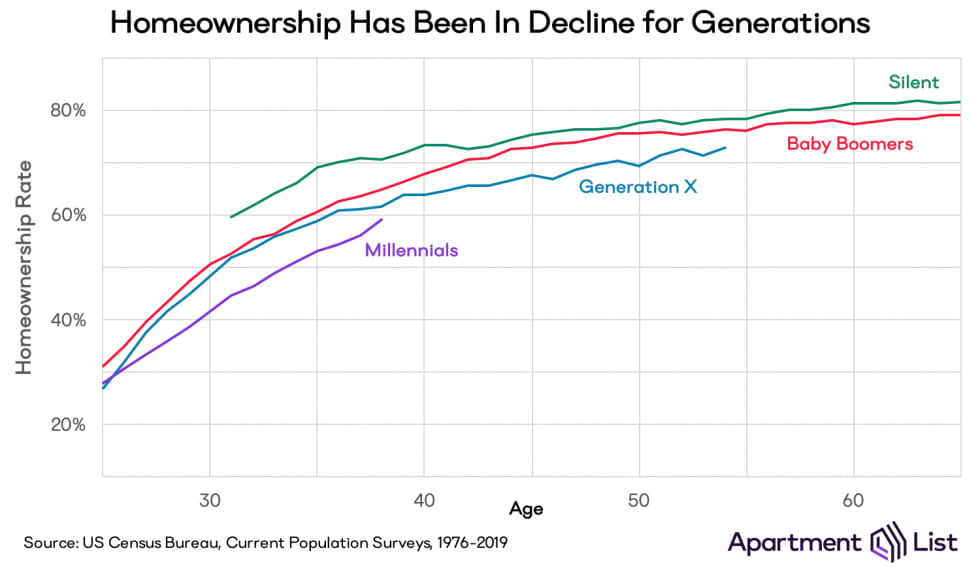

Millennial homeownership is rising, but it is rising slower than it did for previous generations. The chart below compares homeownership rates for each generation as they age. At 25, the millennial, generation X and boomer homeownership rates were all roughly 30 percent. But by 35, after a decade of prime home-buying years, millennial homeownership rose to just 53 percent while generation X and baby boomers reached 60 percent and the silent generation neared 70 percent. 35-year-olds in 1981 (the oldest baby boomers) were nearly 20 percent more likely to own their homes than 35-year-olds in 2016 (the oldest millennials).

Millennials are not the only generation to own fewer homes than their predecessors. In fact, according to the chart above, homeownership has been in decline for at least the last three generations. At age 38, today’s millennial homeownership rate (59 percent) trails the generation X rate (62 percent), which trails the boomer rate (65 percent), which trails the silent generation rate (71 percent).

This highlights a common misconception about millennials: that declining homeownership is a phenomenon unique to them. Their experience was certainly punctuated by the Great Recession, but that recession only accelerated a trend that was already in place for several decades.

In fact, in the coming years millennial homeownership may even catch up to generation X. At age 28, generation X homeownership was six percentage points higher than millennials; by age 38, that gap narrowed to just two. If millennials do eclipse generation X, this would cause a significant change in how we understand millennials, their preferences, and their behavior in the housing market. The narrative would need to shift from millennials being the “generation of renters” to being the first group in half a century to have a higher homeownership rate than the generation that preceded them.

What factors play a role in declining homeownership?

Homeownership for millennials, gen Xers, and baby boomers are all pacing behind their predecessors. Yet the reasons behind this trend may be different for each generation. Below, we dig deeper into three characteristics that are inherently linked to homeownership: income, education, and race.

Income:

Is it high- or low-income households who are buying fewer homes?

For those at the lower end of the income distribution, there is actually little difference between generations.10 Low-income millennials own homes at a similar rate as low-income baby boomers did several decades earlier. For these families, each generation’s homeownership curve is strikingly linear. While high-income households tend to buy most of their homes in their earlier years (giving their homeownership curve its curve), low-income homeownership increases about one percentage point per year, every year. This highlights how owning a home is embedded in the American psyche as a vehicle to economic prosperity. At no age do low-income families give up on their homeownership goals.

The homeownership gap emerges as we move to middle-income households, demonstrating the unique impact of the Great Recession on the millennial and generation X middle-class. Low-income families were mostly priced out of the housing market before the crash, so the recession did not greatly alter their prospects. But middle-class families had homeownership in their sights when they were hit with rising unemployment, wage stagnation, and predatory lending. The recession hit in 2007, when the median-aged millennial was 21 and median-aged gen Xer was 35. These are the inflection points where you see each generation’s middle-income homeownership rate fall behind previous generations.

One could assume that high-income households have the financial means to insulate themselves from the economic forces that affect homeownership. For gen Xers, this appears to have been true; with the exception of some slight separation during their 40s, high-income generation X homeownership tracks closely with baby boomers into their 50s. High-income millennials, on the other hand, have never closed the gap that was widened by the Great Recession. This could signal a combination of economic and cultural shifts, whereby wealthy millennials are now clustering in expensive places where home prices are growing faster than incomes, even for those at the higher end of the income distribution.

Education:

Is the decline in homeownership concentrated among those who did not go to college?

Education serves as a bit of an equalizer between generations; as generations become more educated, their homeownership gaps shrink. Among college-educated 38-year-olds, boomer homeownership is only two percentage points higher than generation X, which is only two percentage points higher than millennials. Conversely, homeownership divides are more pronounced in less-educated households. For 38-year-olds with no more than a high school diploma, boomer homeownership is 64 percent, generation X homeownership is 57 percent, and millennial homeownership is 48 percent.

In other words, the homeownership boost that comes with higher education is much greater for millennials and generation X than it was for baby boomers. For boomers, getting a college education had less of an effect on homeownership. At age 30, the homeownership gap between high-school and college-educated boomers is 7 percent. For generation X it rises to 9 percent, and for millennials it widens to 11 percent.

Race:

Has pressure from the housing market affected America’s racial groups equally?

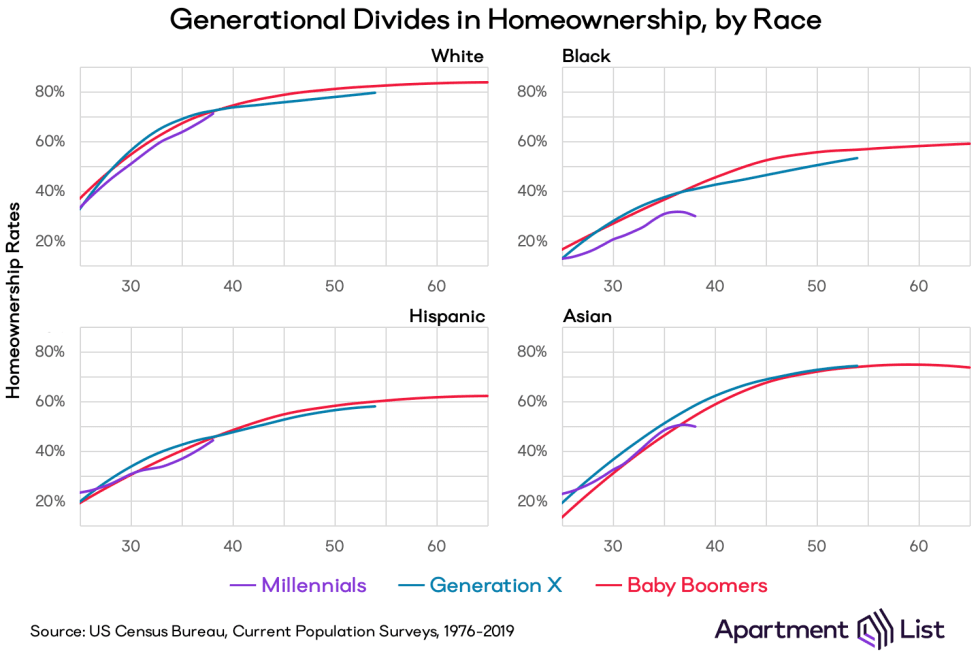

Segmenting our homeownership curves by race11 uncovers a stark reality about millennial homeownership: the generational divide is concentrated in young black households. Black millennial homeownership trails not only previous generations, but also other racial groups. Among the oldest millennials (age 38 in 2019), black homeownership (30 percent) trails asian and hispanic homeownership (49 and 45 percent, respectively), and is a staggering 42 percentage points lower than white homeownership.

For white households, the millennial homeownership gap actually disappears by age 38, when millennials enjoy a slightly higher homeownership rate (72.3 percent) than generation X (71.5 percent) and baby boomers (71.9 percent). Hispanic households show a similar trend, although their homeownership rates are significantly lower: at age 38, hispanic millennial homeownership (44.6 percent) is slightly lower than generation X (45.1 percent) but slightly higher than baby boomers (44.3 percent). Asian households are the only racial group where generation X performed best in the housing market. At age 38, asian generation X homeownership (56.3 percent) exceeds both boomers (54.0 percent) and millennials (49.2 percent).

Conclusion: Looking Ahead to Gen Z

Homeownership is often—and incorrectly—framed as a story about baby boomers who had it easy versus millennials who have it rough. The reality is much more nuanced. The millennial experience is not an isolated event, it is the continuation of a downward trend in homeownership that started decades ago. Beginning with the silent generation, each subsequent generation has purchased homes at a slower velocity than the one that preceded it. But as the economy has strengthened since the Great Recession, millennial homeownership has risen quickly. They are often characterized as the generation that was excluded from the housing market, but it is possible that their homeownership rate will eclipse that of generation X in the near future.

Born 1997 and later, generation Z is just now entering the housing market. But predicting their behavior is difficult. Many of the forces that make homeownership challenging for earlier generations show no sign of slowing down. Homes remain expensive and under-supplied in major markets, rising student debt continues to impede mortgage savings, and young Americans continue to delay starting families. Furthermore, a decade of strong economic growth—one that improved homeownership opportunities—has come to an abrupt end in 2020. Just as the Great Recession was a watershed moment for millennials, the coronavirus pandemic seems poised to have a significant impact on generation Z. Their homeownership rate will depend heavily on the nation’s ability to rebound from the crisis. If a long recession ensues, generation Z homeownership may suffer and continue the trend set forth by earlier generations.

- US Census Bureau, 2019 Current Population Survey.↩

- HousingWire: Millennials Have Officially Entered the Housing Market↩

- Wall Street Journal: Millennial Home Buyers Might Never Come Knocking↩

- HousingWire: Homeownership rate rises to four-year high as Millennials are finally buying homes↩

- Business Insider: Homeownership across America is on the decline for the first time since 2017, and millennials are partially to blame↩

- Forbes: Are Millennials Killing the U.S. Housing Market?↩

- Business Insider: 8 ways American millennials are changing homeownership↩

- Many recent studies equate millennials with 25-34 year olds. This is done mostly out of convenience, as it aligns with age brackets that the Census Bureau publishes. But approximating generations with static age bands becomes problematic if you want to track generations over time. For instance, in the coming years, "25-34" will comprise a blend of younger millennials and older members of generation Z.↩

- For this study we use data from the Census Bureau's Current Population Survey. Here homeownership is a household-level variable, so one household can contain members of multiple generations. We attribute each household a generation according to the "householder," defined as "the person in whose name the home is owned, being bought, or rented."↩

- Low-, middle-, and high-income refers to households in the fifth, third, and first income quintiles for a given year, respectively.↩

- These groups do not include households in which the head is classified "other" or "two or more races." This group represents a larger share of millennials (1.8%) than gen Xers or boomers (0.9% each), but remains a small fraction of households.↩

Share this Article