American Dream of Homeownership Delayed for Millennial Generation

In a nationwide survey of about 24,000 renters Apartment List found that the 80 percent of millennial renters, born between 1982 and 2004, want to purchase a house or condo, but face a huge obstacle: affording a home. For some millennials that means a wait of at least two decades before they can afford to buy a home.

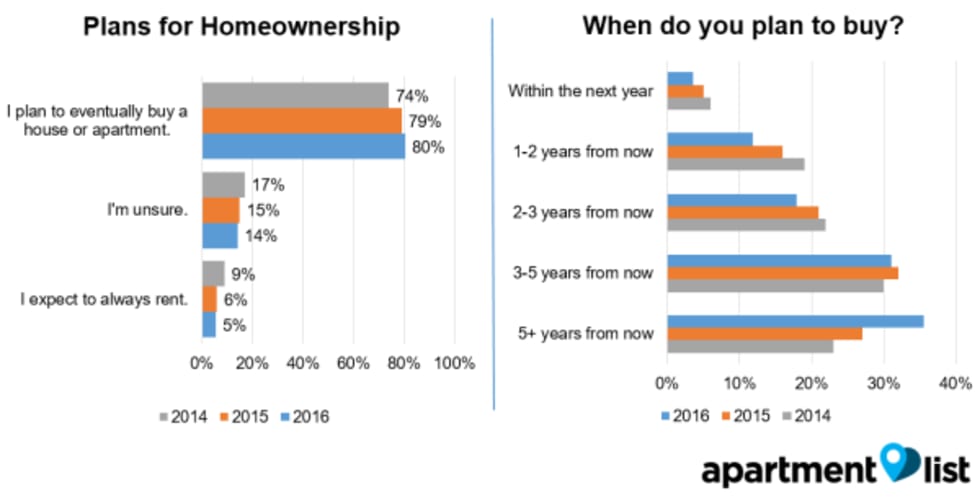

Despite the overwhelming desire to own, millennials from Los Angeles to New York and everywhere in between, surveyed from October 2016 through April 2017, revealed they are increasingly delaying their plans for homeownership. 16 percent of respondents said they plan on purchasing a home within the next two years, compared to 25 percent in our 2014 survey. Meanwhile, about two of three respondents, or 67 percent, said they expect to wait three years or more, an increase from about 53 percent in the 2014 survey.

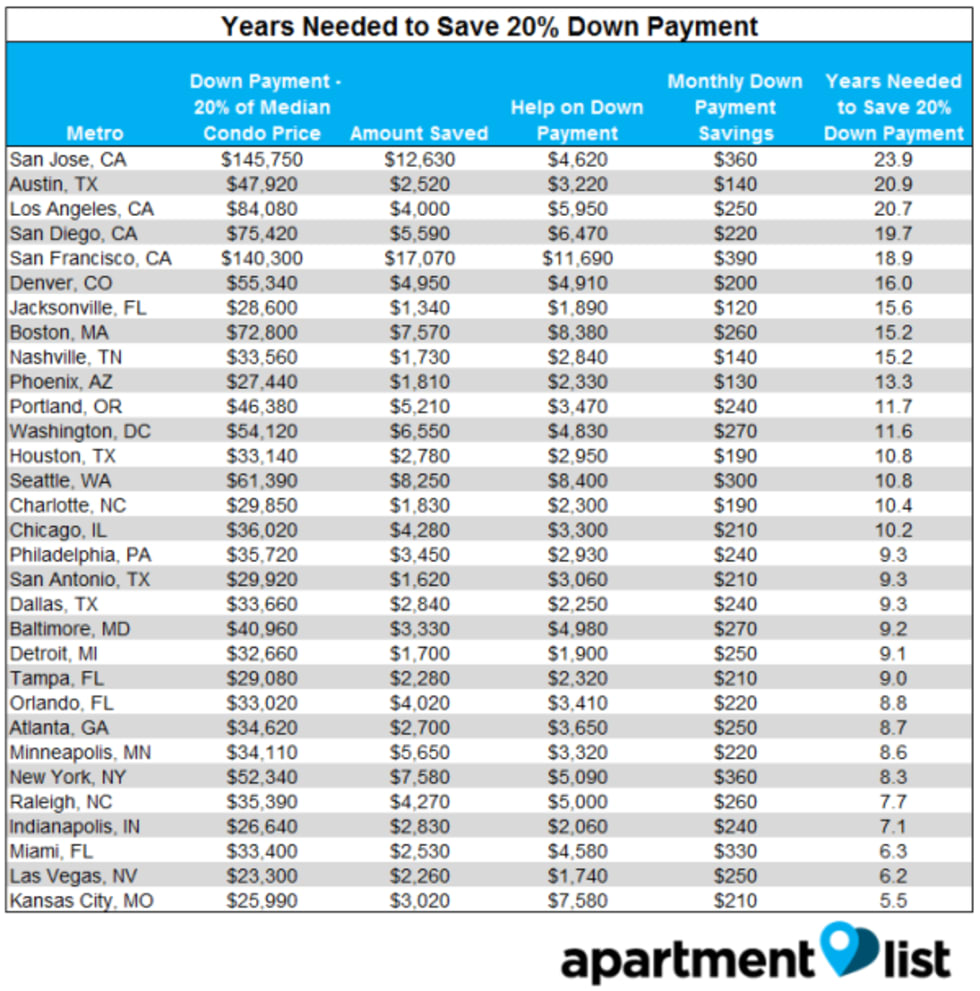

Based on their current rate of monthly savings, our survey found that millennials in many of the nation's large metros will need at least a decade to save enough money for a 20 percent down payment on a condo. Millennials in San Francisco, San Diego, Los Angeles, Austin and San Jose each face a wait of at least 19 years. A millennial in San Jose, the metro with the longest wait time of almost 24 years, wouldn’t be able to afford a 20 percent down payment on a condo until the year 2041. Millennials in Kansas City need the least time to save for a down payment: five and a half years. Even if we assume a smaller down payment of 10 percent, just over one in three millennials will be able to save the required amount in five years or less.

These results underscore the long-term crisis that home ownership in the United States may face, as millennials delay buying a home until later in life. One of the outstanding questions for the housing market has been whether or not the nation’s largest generation--millennials--will purchase homes at rates similar to their parents or if they will continue to rent long into adulthood, or even indefinitely.

Recently, there have been some encouraging signs that more new home buyers are entering the market, with new-owner households outnumbering new-renter households and the share of first-time buyers slowly increasing. That said, the homeownership rate for those under age 35 has not shown significant signs of recovery. It currently stands at 34.3 percent, which is essentially flat in comparison to this time last year and well below pre-recession levels, when it hovered around 43 percent.

Despite recent improvements in the labor market, millennials face a severe shortage of affordable entry-level homes in many parts of the country. This leaves millennials with difficult choices: extend their budgets and purchase at higher debt-to-income ratios, heightening the risk of mortgage default; migrate to more affordable areas; or delay buying a home altogether.

Homeownership has traditionally been a key component of the American Dream, and the primary driver of wealth creation for many families. However, in the aftermath of the housing market collapse in 2008, the U.S. homeownership rate has fallen to historic lows and, despite recent leveling off, has not shown signs of recovering to its pre-recession peak.

High levels of student debt and stagnant career opportunities have long kept millennials sidelined from the real estate market and, even with recent improvements in the labor market, affordability continues to be a major concern. Our analysis shows that the lack of savings by millennials, combined with the extreme shortage in affordable entry-level homes, means that a large share of millennials may be stuck renting for years.

‘Why Are You Waiting to Buy a Home?’

In this survey, respondents were asked the following questions:

- Do you plan to buy a house or condo in the future?

- How soon do you expect to be buying a home?

- Why are you waiting to buy a home?

- How much do you expect to need for a down payment?

- How much do you have saved for a down payment so far?

- How much help (e.g., from family) will you be receiving for a down payment?

- How much of your monthly income do you put towards saving for a down payment?

We combined survey results with 2016 data from the National Association of Realtors on the median apartment condo sales price in metros across the country, and we used those figures as a proxy for starter home prices for millennials. We assumed a 20 percent down payment on that price and compared this to respondents’ self-reported expected down payment. We also calculated the number of years that respondents will need to save a down payment, based on current savings levels and monthly savings rates.

Millennials Increasingly Delaying Homeownership Dream

The 80 percent of respondents who indicated they plan to eventually buy a house or apartment contradicts a popular notion that millennial preference for living in dense, walkable urban areas makes home ownership less attractive to this generation. That percentage has been inching higher from the 74 percent that said they plan on eventual home ownership in 2014 and 79 percent in 2015, but the figure has been relatively consistent over the past three years of our study.

However, the length of time millennials plan to wait before purchasing has been increasing over the three years of our study. In our 2014 survey, just 23 percent of respondents said they plan to wait five years or more, but that figure has since increased by more than half, and now stands at 36 percent.

Breaking the Bank: Affordability is Primary Obstacle

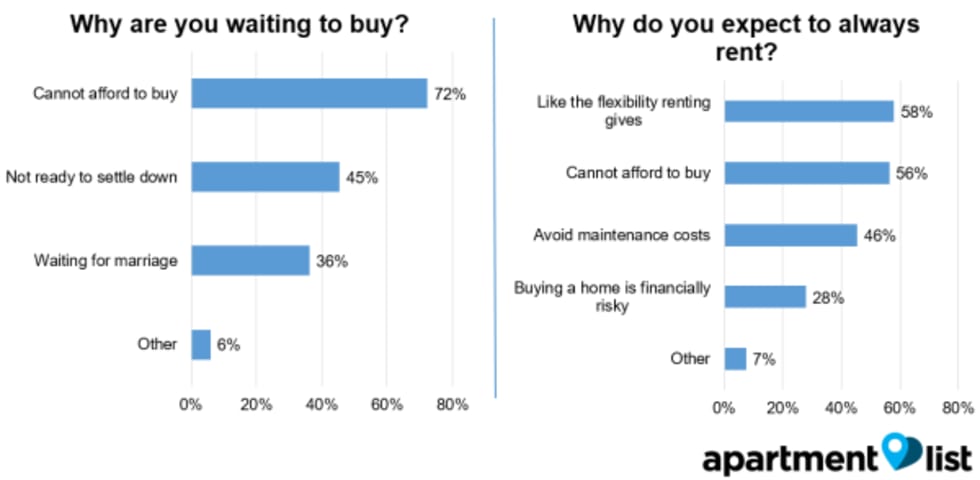

Of those respondents who plan to purchase a home in the future, some 72 percent said affordability is the primary obstacle, slightly down from 77 percent in last year’s survey. Almost half, or 45 percent, said they are not ready to settle down, while about one of three respondents, or 36 percent, said they are waiting to get married. Respondents could choose multiple answers to this question.

Among renters who do not plan to buy, the most popular reason, among 58 percent of respondents, is that they enjoy the flexibility of renting. However, nearly as many, or 56 percent, cite affordability.

Waiting to Get Hitched: College Educated Less Ready to Settle Down

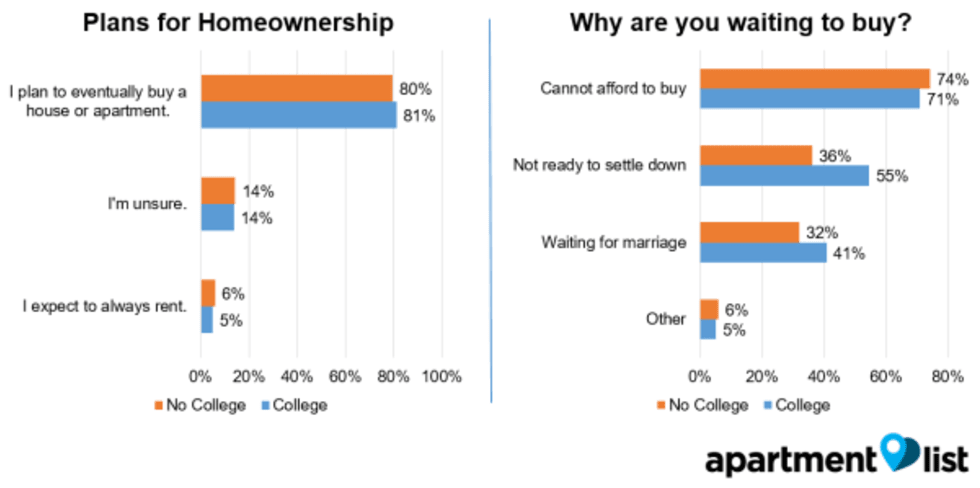

Based on education levels, there wasn’t a significant difference in homeownership plans among respondents, with 81 percent of those who attended college planning to purchase a home and 80 percent of non-college educated respondents having similar plans. Affordability is also the most significant obstacle for both groups. About 74 percent of those without college degrees cited affordability as an obstacle, as did 71 percent of respondents with college degrees.

However, we saw a significant divergence when it came to another question: readiness to settle down as an obstacle. About half, or 55 percent, of those who attended college cited this as an obstacle to homeownership, compared to just about one of three, or 36 percent, of the group without a college degree. There was a similar, though less stark, disparity when asked if waiting to get married or finding a long term partner was an obstacle to purchasing a home.

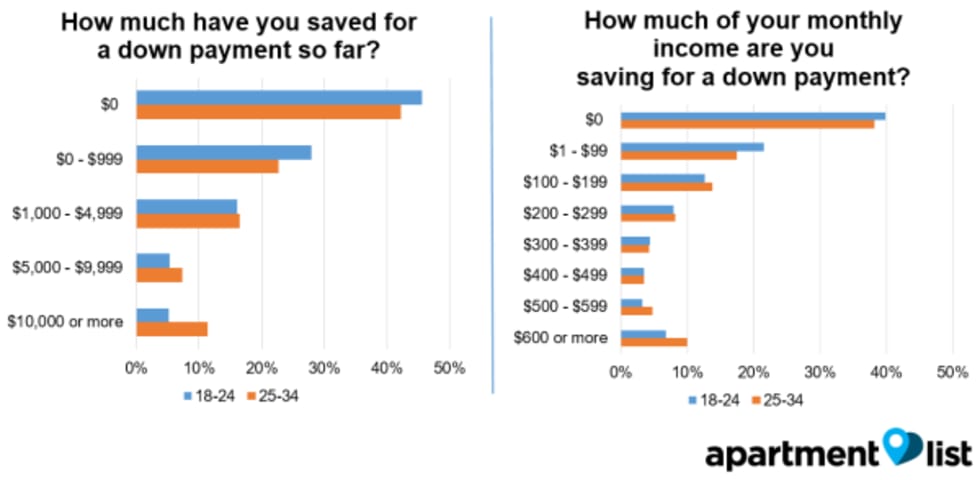

Over Two-Thirds Have Less Than $1,000 in Down Payment Savings

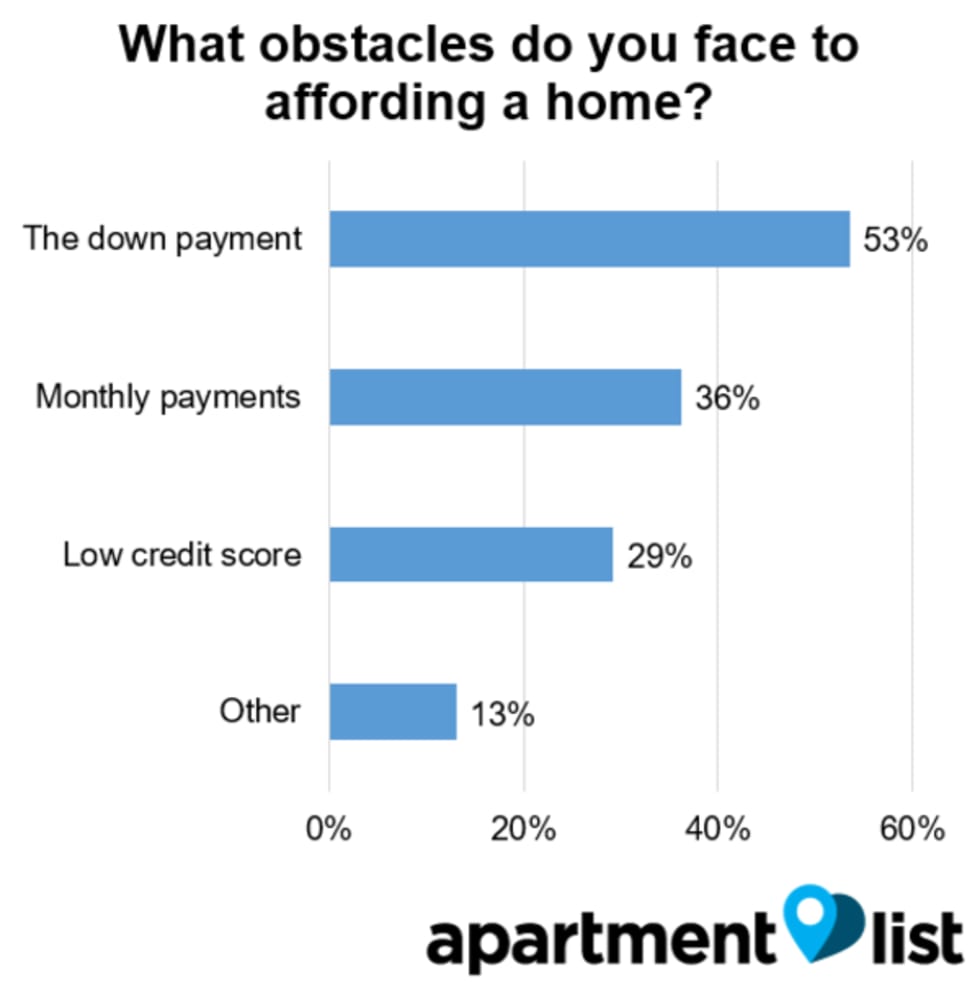

Given that affordability is of primary concern across the board, we looked at how millennials are preparing financially for homeownership. While around one of three respondents have concerns about their credit scores and their ability to afford monthly mortgage payments, the biggest concern is having enough money for a down payment, an obstacle for more than half of millennial renters.

68 percent of millennials said they have saved less than $1,000 for a down payment. Almost half, or 44 percent, of millennials said they have not saved anything for a down payment. Nearly the same amount, or 39 percent, said they aren’t saving for a down payment on a monthly basis. Only 15 percent have saved $5,000 or more, and only 29 percent are saving $200 or more each month.

Older millennials, 25 to 34 years of age, were twice as likely to have saved $10,000 for a down payment, but almost half of them, or 42 percent, also said they haven’t saved toward a down payment.

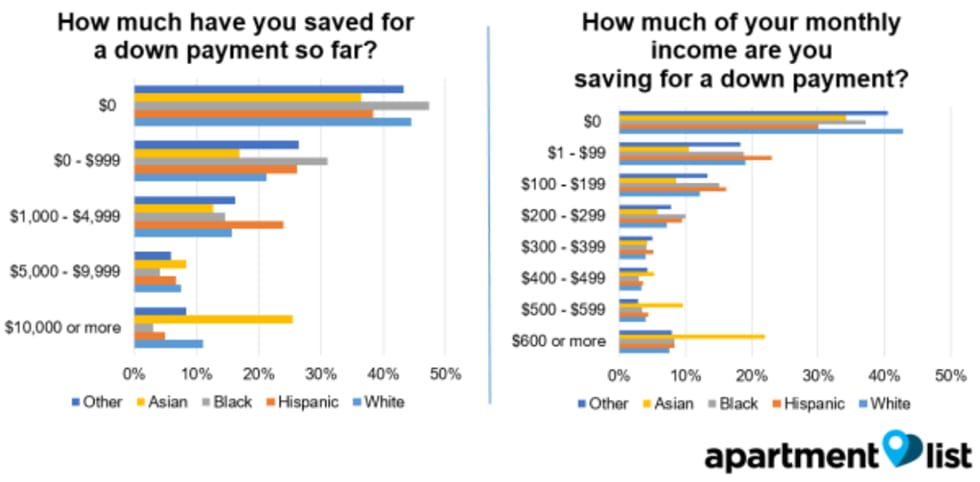

Asian Millennials are Most Financially Prepared

Across the board, more than a third of respondents of all races--Asian, black, Hispanic and white-- said they haven’t saved anything toward a down payment. However, almost one of four, or 26 percent, of Asian respondents said they had saved more than $10,000 for a down payments, well over double the share of any other race. Asian respondents were also far more likely to be saving $600 or more toward a down payment each month.

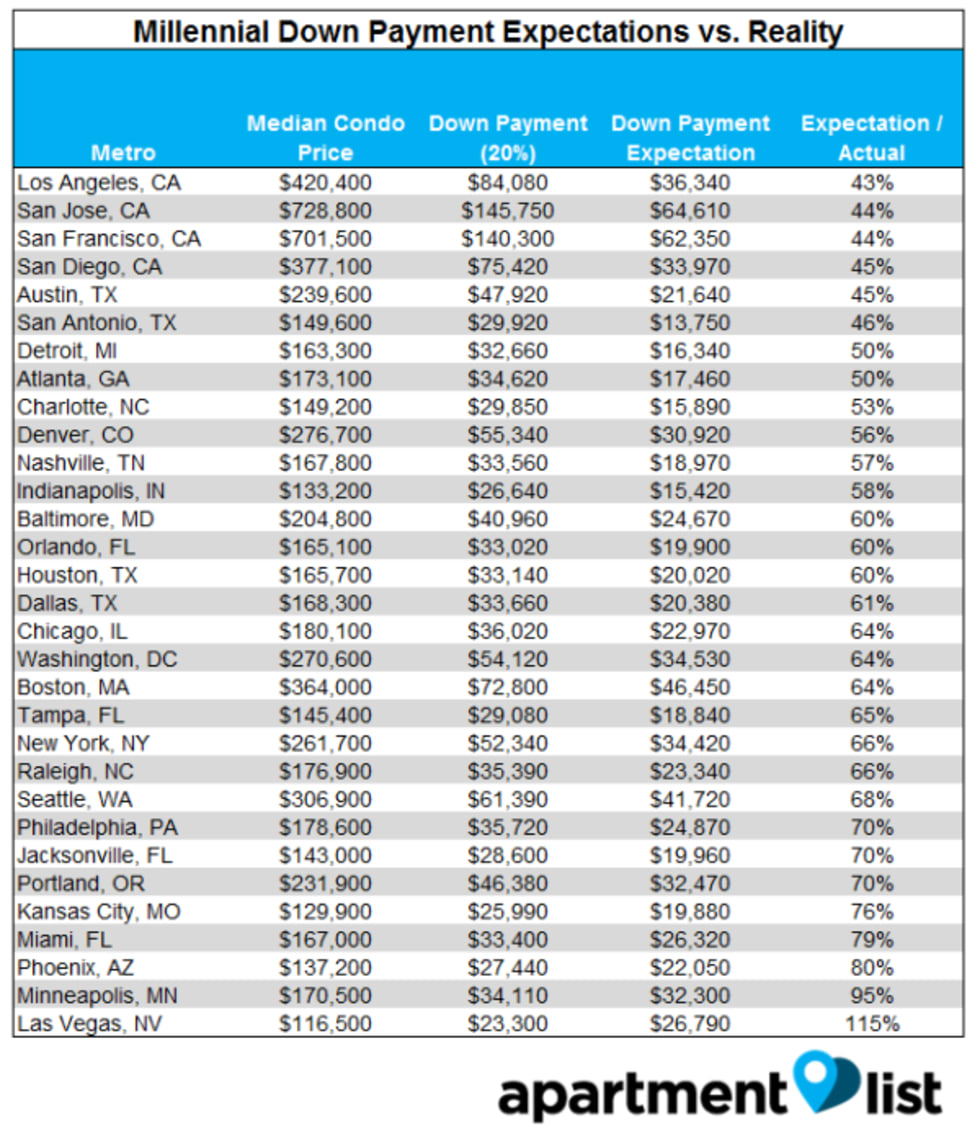

Expectation Gap: Millennials Underestimate Down Payment Needed

Further complicating matters, millennials seem to have an expectation that they need a lot less for a down payment than they actually do. For example, in Los Angeles, the market with the widest gap in expectation and reality, the actual median price of a condo is $420,400, meaning that a 20 percent down payment comes out to $84,080. Respondents in that region estimated that they will need $36,340, which is less than half of the actual amount.

Even in more affordable metros like Detroit, where the median price of a condo is $163,300, a 20 percent down payment would be $32,660, but millennials in that region said they expect to have to pay just $16,340.

In Many Metros, a Decade or More Needed to Save a Down Payment

Based on the average of respondents’ current down payment savings, the amount of help they expect to receive and the amount they’re saving on a monthly basis, we calculated the number of years millennials would need to amass a 20 percent down payment. Our calculation accounts for growth in home prices and wages, as well as returns on savings. We have assumed that home prices will increase at the historical average growth rate over the past 20 years. We make a similar assumption for wage increases, and assume that as their incomes grow, renters will continue put the same percentage toward down payment savings. Finally, we assume that renters will earn a return on their savings equal to the average growth of the S&P 500 over the past 20 years.

The results are staggering. Millennials in over half of the metros we looked at will need at least a decade to save for a down payment, and in some of the costliest West Coast cities, they will need nearly two decades or more. Of course, it is possible to purchase a home with less than a 20 percent down payment, although mortgages with lower down payments often come with higher interest rates and mortgage insurance premiums. However, even if we assume a 10 percent down payment, many millennials still have a long way to go.

Nationally, only 15 percent of millennials aged 25 to 34 will save enough for a 10 percent down payment within the next year, and nearly two-thirds of respondents will need more than five years of saving at their current rates to amass that amount.

Given these results, it seems that, despite aspiring to purchase a home, millennials in many cities are many years away from being able to actually afford to do so. It’s possible that increased wage growth will allow millennials to accelerate their savings in the coming years or that millennials in the most expensive markets will migrate to more affordable areas as they prepare to settle down, but based on their current financial statuses, it seems unlikely that millennials will begin purchasing homes en masse in the near-term future.

Share this Article