Missed Payments Stabilize In June -- At Alarming Levels

- In June, 30 percent of Americans missed their housing payments, down slightly from 31 percent in May but still up from 24 percent in April.

- Missed payments continue to concentrate among renters, younger and poorer Americans, and those who cannot work remotely.

- A majority of payments missed at the beginning of the month are paid by the end of the month. But those who do not pay on-time in one month are much more likely to miss a payment in the following month.

- Some eviction and foreclosure protections are beginning to expire, creating concern that many Americans will soon lose their housing as a result of missed payments. 37 percent of renters (and 26 percent of homeowners) are at least somewhat concerned that in the next six months they will face an eviction or foreclosure.

Introduction

As the U.S. enters its fourth month of adapting to the COVID-19 pandemic, many economic indicators are beginning to turn the corner. By June 1, most states had started reopening their economies. After the nation lost over 20 million jobs in April, 2.5 million were added in May as laid off workers began returning to their jobs.1 Have rent and mortgage payments started to rebound as well?

To understand the pandemic’s ongoing effect on housing affordability, our team has surveyed thousands of Americans about their ability to make monthly housing payments over the past three months.2 This month the rate of missed payments is similar to what we observed last month, indicating that while the pandemic’s impact on affordability has begun to stabilize, the situation has not yet improved meaningfully. 30 percent of Americans have yet to pay their June rent or mortgage bill in full. This rate remains historically high, but the one-percentage point reduction from last month may signal that the worst is behind us.

3 in 10 Americans Missed Their Housing Payments in June

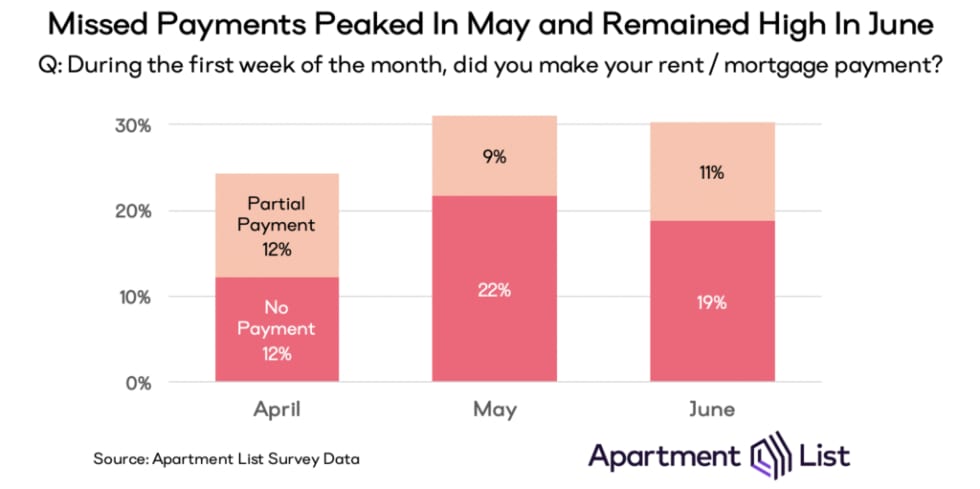

The missed payment rate—the percentage of renters and mortgaged homeowners failing to make a full payment at the beginning of the month—jumped to 24 percent in April, rose again to 31 percent in May, and then dipped slightly to 30 percent in June. Of those who have yet to make their June housing payment, one-third made a partial payment and two-thirds made no payment at all.

This hardship continues to be concentrated among renters, younger and lower-income households, and urban dwellers. Missed payment rates are highest for renters (32 percent), households earning less than $25,000 per year (40 percent), adults under the age of 30 (40 percent), and those living in high-density urban areas (35 percent). While the missed payment rate for mortgaged homeowners is just 3 percentage points lower than renters, the data indicate that homeowners are getting more assistance from their lenders than renters are from landlords. Our survey asks which concessions (e.g., deferred or reduced payments), if any, are being made to assist with housing costs. Each month about 40 percent of renters who make less than a full payment say they made some such arrangement with their landlords. But for homeowners in a similar situation, the percentage who received a concession has steadily ticked up: from 44 percent in April to 47 percent in May to 53 percent in June.

Since the onset of the pandemic, our team has explored the dramatic effect of remote work on short-term housing affordability and broader economic inequality. Remote jobs boast higher wages and were less likely to be disrupted by the mandatory quarantines that swept the nation earlier this year. Months later, remote workers are continuing to benefit from their workplace flexibility. Those who are able to work remotely full-time are least likely to have missed their June housing payment (21 percent). The highest rate actually falls on those who say they can do some, but not all, of their job responsibilities from home; 19 percent of these workers made no June payment and an additional 22 percent made a partial payment. Among those who cannot work from home at all, one-quarter have missed their June housing payment altogether, more than any other group surveyed.

Despite many households missing payments at the beginning of each month, the majority have managed to close the gap with late payments over the following weeks. In April, nearly one quarter did not make a full on-time payment, but fewer than 10 percent remained delinquent by the end of the month. May showed a similar trend: the missed payment rate dropped from 31 percent at the beginning of the month to 11 percent at the end.

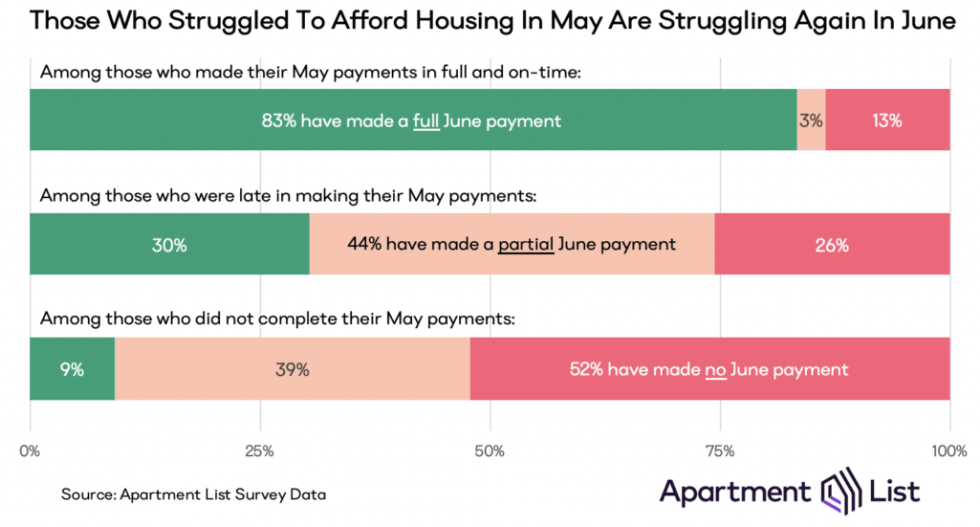

Delayed payments in one month are a strong predictor for missed payments in the next. 83 percent of those who paid their May housing in full and on-time did so again in June, but only 30 percent who were late in May have made their full payment this month. The June payment rate dips below 10 percent for those who never finished their housing payments.

What Happens Next?

Despite the discouraging numbers over the past three months, many Americans have had an important safety net: an outright ban on evictions and foreclosures due to missed payments. In March, the federal CARES Act extended this protection to residents of public housing and homeowners with federally-backed mortgages (as well as their tenants). State and local governments followed suit, extending moratoria to additional renters and homeowners not covered by the federal law. In June, however, despite the fact that Americans financially affected by coronavirus are still struggling to pay their bills, many of these eviction and foreclosure protections are expiring, giving landlords and lenders the opportunity to file claims against unpaid bills.

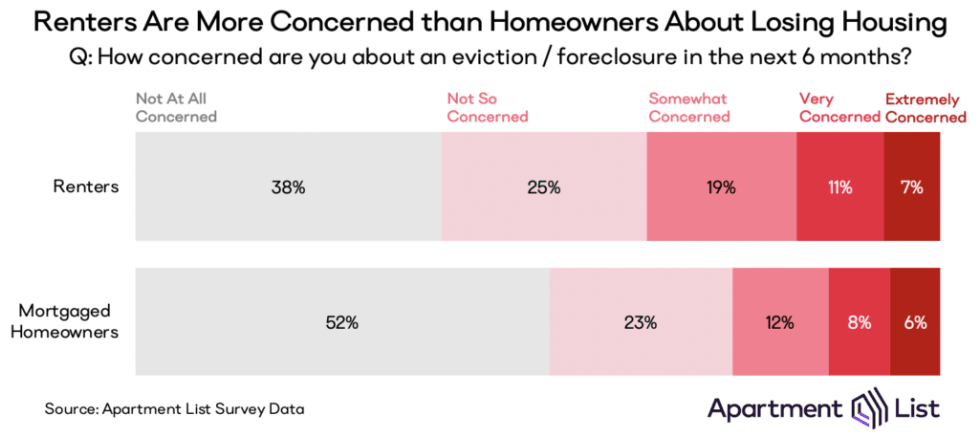

As a result, there is a growing concern that eviction notices will swell in the coming months, forcing families out of their homes at a time when they are most financially vulnerable. Our survey finds that over one-third of renters are at least “somewhat concerned” that they will be served an eviction notice in the coming six months. That number jumps to a staggering 56 percent among those who have not yet paid their full rent for June. Eviction concern is also elevated among low-income renters (48 percent), those living in dense urban areas (47 percent), and those without the luxury of working from home (41 percent).

A large percentage of mortgaged homeowners are also feeling the pressure; just over one-quarter are at least somewhat concerned their homes will be foreclosed on in the coming six months. Foreclosure concern is greatest among homeowners under 30 (48 percent), indicating that first-time homeowners may be feeling disproportionate strain. Other groups with elevated foreclosure concern include those with household incomes below $25,000 (52 percent), and those living in dense urban areas (47 percent).

Even as June’s economic indicators show signs of improvement, the speed of the economy’s rebound still depends critically on the spread of COVID-19 and policy initiatives at the federal and local level. As economies reopen, many families find themselves facing a new economic reality with new housing preferences. The recovery will be long and uneven, but in the meantime, the affordability concerns that were bubbling throughout boom times are boiling over in times of crisis.

- Source: U.S. Bureau of Labor Statistics. Economic News Release, June 5, 2020.↩

- As with our April and May surveys, in June we again partnered with SurveyMonkey to collect over 4,000 responses across a panel of respondents that match the gender and age distribution of the United States as a whole.↩

Share this Article