Not really a renter, definitely not a homeowner: over 9 million young adults are stuck somewhere in between

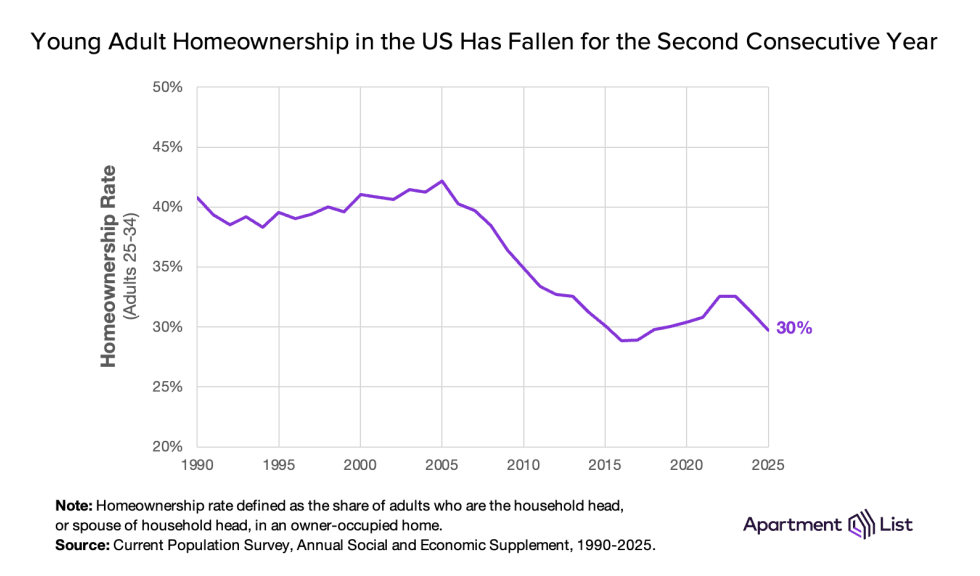

Homeownership among young adults has fallen to just 30%

A recent analysis by our team shows that the individual homeownership rate in the United States – the share of adults who are the household head, or spouse of household head, in an owner-occupied home – has fallen for two consecutive years and wiped out gains that were steadily accumulated between 2017 and 2022. This reversal is even more dramatic among young adults ages 25 to 34, who amid a major affordability crunch have seen their homeownership rate fall to just 30 percent nationwide.

Since 2020, a sequence of financial hurdles have hit the housing market and pushed homeownership out of reach for many young people. First, sales prices skyrocketed in 2020-21 when a sudden wave of pandemic-related moves drove up demand for single-family homes. Higher interest rates followed in 2022, stalling price growth but driving up monthly payments for new mortgages. Since then, insurance premiums, utility prices, and other costs associated with homeownership have risen sharply. Both the upfront and recurring costs of homeownership are significantly higher today than they were five years ago.

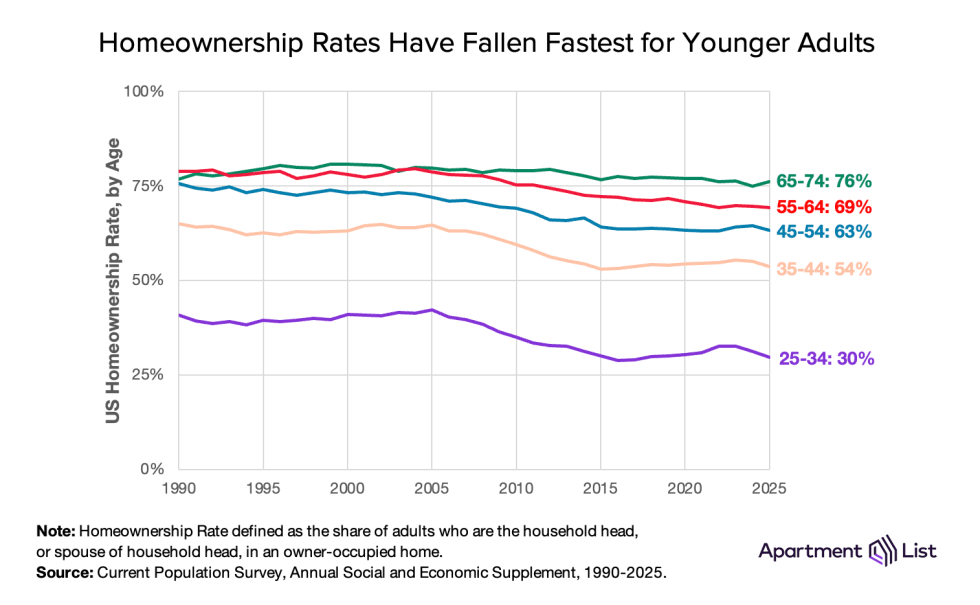

These hurdles have been particularly challenging for younger adults. For those ages 25 to 34 – historically prime years for first-time homebuying as people settle into their careers, get married, and start families – the homeownership rate has fallen just to below 30 percent and is approaching the recent low set in 2017, when it bottomed out after a decade-long slide spurred by the Great Financial Crisis. During the past two years homeownership has fallen across all age groups, but the decline has been most pronounced for young adults.

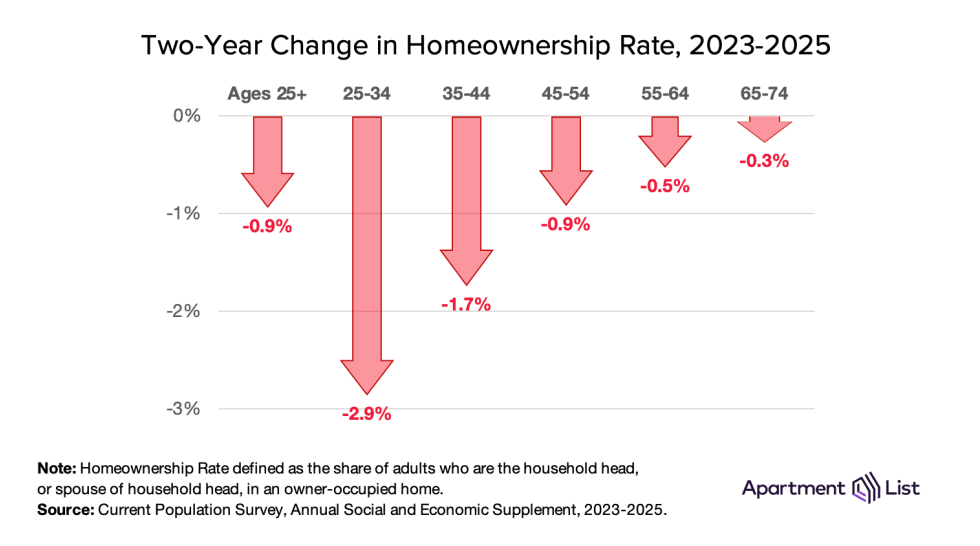

From 2023 to 2025, the nationwide homeownership rate fell nearly a full percentage point. The decline among young adults is over triple that amount, with their homeownership rate sinking 2.9 percent. Homeownership fell 1.7 percent for ages 35 to 44, 0.9 percent for ages 45 to 54, 0.5 percent for ages 55 to 64, and just 0.3 percent for ages 65 to 74.

Amid rising costs, more young adults are renting or living in someone else’s owned home

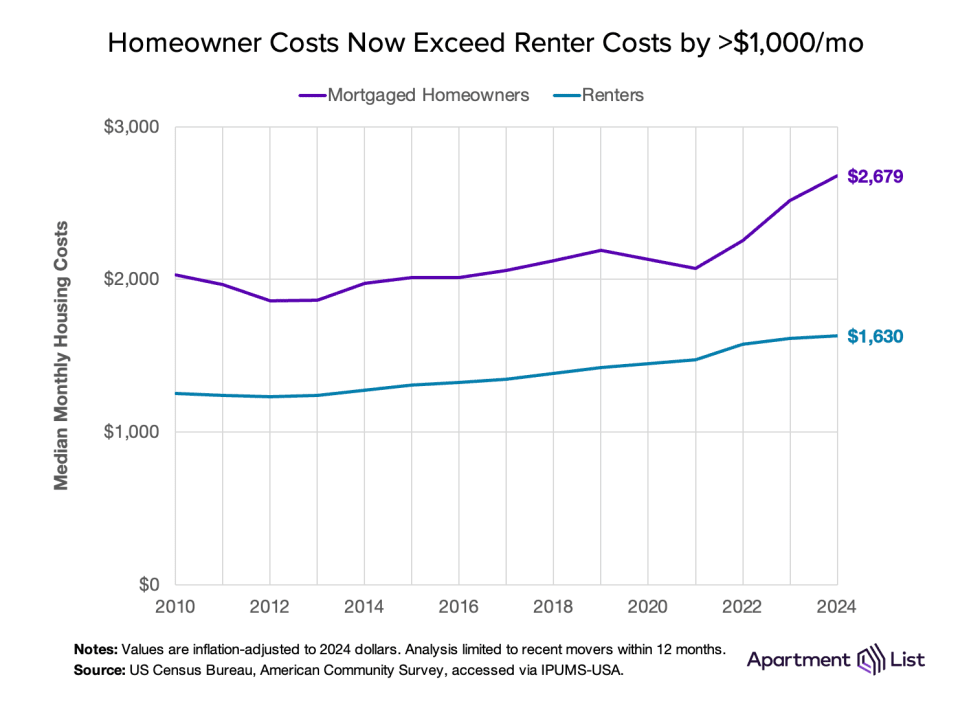

The high cost of homeownership is frequently cited as a boon to the rentals industry, because when homeownership is financially out of reach, people will rent for longer. Today’s rental market, facing high vacancy rates and a historic wave of new construction, is largely propped up by this steady demand for renting as the only financially-available choice. Monthly housing costs are over $1,000 more per month for new homeowners than for renters, and the gap has widened substantially since 2020. In some markets, homeowners are spending more than twice as much on housing than renters.

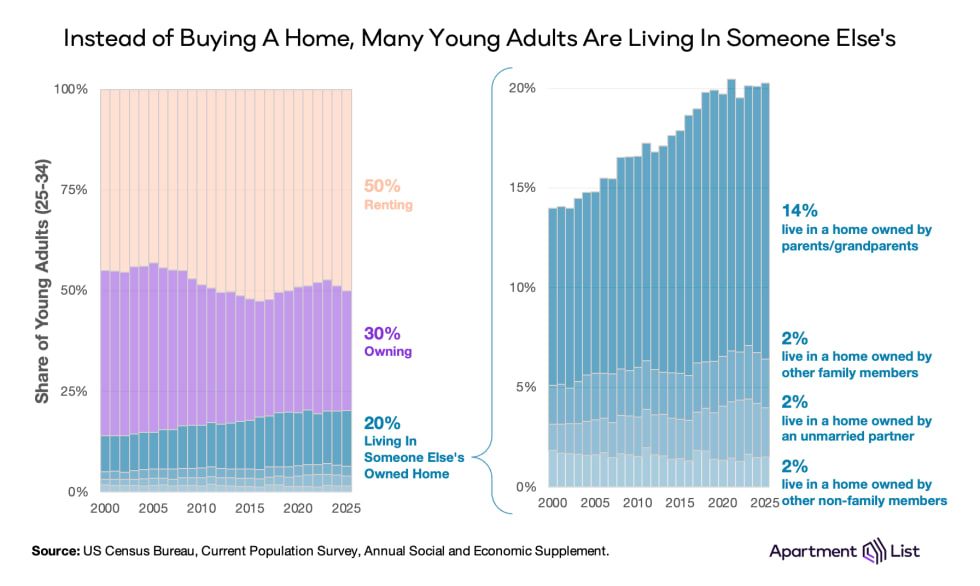

Accordingly, 50 percent of young adults now rent. Their rental rate is approaching a new high just as their homeownership rate approaches a new low. But renting has also gotten more expensive; since 2010, the inflation-adjusted median rent for recent movers has increased by 30%. With both homeownership and renting becoming increasingly financially burdensome, millions of young adults are now choosing a third option: foregoing homeownership as well as renting in the traditional sense, and instead living in someone else’s owned home.

Today, 20 percent of young adults between 25 and 34 (totalling more than 9 million individuals) live in someone else’s owned home, a rate that has steadily risen from 14 percent in 2000. The majority of this group lives at their parents’ or grandparents’ house. Reasons for doing so vary, but for some this appears a strategy for affording homeownership, as the group of young adults living at home actually shrunk during the early-pandemic homebuying spree. But since then the group has resumed growing quickly; today an all-time high of 6.3 million young adults live in a home owned by their parents or grandparents. The remaining 3 million live in homes owned by other family members, or non-family members like friends or unmarried partners.

Young adult homeownership is lowest in California

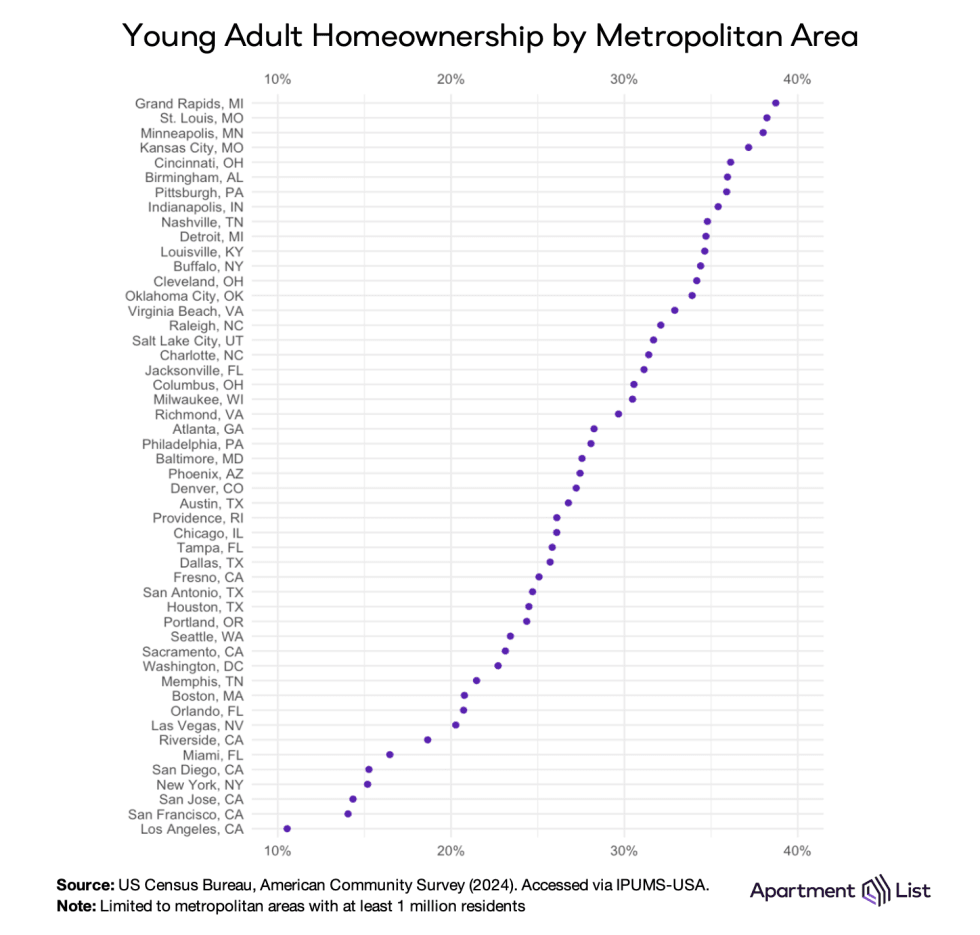

Not surprisingly, the nation’s most expensive housing markets are the ones where young adults have the lowest rates of homeownership. At the bottom of the list is Los Angeles metro, where just over 10 percent of adults between the ages of 25 and 34 are homeowners. It is a similar story in other California markets, including San Francisco and San Jose metros (14 percent), San Diego metro (15 percent), Riverside metro (19 percent), and Sacramento metro (23 percent). Expensive metropolitan areas like New York, Miami, Boston, Washington DC, and Seattle also find themselves towards the bottom of the list.

On the other end of the spectrum, young adult homeownership is higher in lower-cost markets across the nation’s midwest and southern states. Grand Rapids metro has the highest rate (39 percent), followed by St. Louis and Minneapolis metros (38 percent), Kansas City metro (37 percent), and Cincinnati, Birmingham, and Pittsburgh metros (36 percent). Fewer adults in these markets live in someone else’s owned home, signalling that both homeownership and renting are more accessible options for young adults.

Will young adult homeownership get better before it gets worse?

Similar to the rental market, the for-sale housing market is showing some signs of softening. According to the Case-Shiller Home Price Index, which monitors home prices in a similar manner as our rent model, price growth has slowed from 6 percent in 2024 to 1 percent today. And in several high-construction markets like Dallas, Phoenix, and Denver, home prices are down 2 percent year-over-year. Active for-sale listings are also trending up, albeit slowly. The for-sale market is showing gradual improvements in affordability, but not enough to close the homeowner-renter cost gap and make a meaningful difference for young adults eyeing their first mortgage. Labor market uncertainty has also curtailed wage growth for everyone but the highest earners, making it difficult for renters (or those living at home) to bridge the gap to homeownership.

Share this Article